Auto insurance is increasingly being priced on assumptions that no longer hold. Vehicle usage is becoming more variable, exposure less predictable, and customers more sensitive to paying for coverage they do not fully use. As this gap widens, it creates both a pricing risk and a retention risk for carriers still anchored to fixed annual models.

Usage-based and on-demand insurance models are emerging as a direct response. According to research, the global usage-based insurance market is projected to grow from roughly $43 billion to over $70 billion by 2030.

According to McKinsey, more than 40% of U.S. auto insurance customers express interest in usage-based or behavior-linked pricing models. As demand accelerates for pricing models tied to mileage, driving behavior, and flexible activation, insurers face a more important question than whether on-demand models are gaining traction: which models are commercially viable, operationally feasible, and worth scaling. Not all on-demand structures solve the same problem. Some work as acquisition tools, some sharpen underwriting precision, and others support retention in rate-sensitive segments.

What Is On Demand Auto Insurance?

On demand auto insurance refers to coverage that is activated, priced, or adjusted based on time, usage, behavior, or context rather than fixed annual assumptions. Instead of locking in a 12-month exposure period, the policy structure responds dynamically to how and when a vehicle is used.

In practical terms, this includes temporary car insurance for short durations, usage based auto insurance tied to mileage, telematics insurance driven by driving behavior, subscription car insurance bundled with services, embedded auto insurance offered at the point of vehicle purchase, and on-off activation models that allow policyholders to toggle coverage.

What distinguishes on-demand models from traditional personal auto is not simply flexibility, it is pricing logic and operational design. Premium is linked more closely to exposure data. Underwriting increasingly relies on real-time inputs. Servicing is digital-first. Proof of insurance, regulatory disclosures, and state reporting often must occur instantly.

For U.S. P&C insurers, this introduces structural implications. Rating engines must support micro-duration logic. Fraud controls must operate at bind. Compliance workflows must align with state-specific rules on cancellation, cooling-off periods, minimum limits, and proof-of-coverage timing. On demand auto insurance is therefore less a single product and more a category of portfolio strategies built around responsive exposure measurement.

5 Types of On Demand Auto Insurance

1. Pay As You Need (Time-Based Cover)

Pay As You Need, or time-based cover is a form of temporary car insurance that provides protection for a defined short duration, typically hourly, daily, or weekly. Coverage activates for a specific time window and expires automatically at the end of that term.

Unlike a traditional policy that simply gets cancelled early, time-based on-demand cover is intentionally engineered for limited exposure. That matters because short-duration buyers are often selecting coverage around specific moments, which can create very different loss patterns than a stable annual book. Pricing therefore reflects compressed duration risk and higher variance, rather than spreading expected loss across a full-year premium base.

Best-Fit Customer Segments for Pay As You Need Model

- Borrowed car drivers

- Occasional drivers who do not maintain full-time policies

- Urban residents using vehicles intermittently

- Short-term vehicle access (weekend travel, road trips)

- Gig drivers during temporary activation windows

This model often appeals to digitally comfortable consumers who expect immediate coverage confirmation and proof of insurance.

Strategic Value for Insurers

Time-based cover can serve as:

- A low-friction acquisition channel for younger or first-time insureds

- A bridge product that converts short-duration users into annual policies

- A way to participate in non-owner or occasional-driver segments

- A defensive play against insurtechs specializing in temporary car insurance

For carriers with strong direct-to-consumer capability, this model can also reinforce brand relevance among mobility-first demographics. Strategically, it expands the addressable market without immediately committing to long-term exposure.

2. Pay As You Go (Mileage-Based Coverage)

Pay As You Go is a form of usage-based auto insurance where the premium is directly linked to miles driven. Instead of paying a fully fixed annual premium, the insured typically pays a base rate plus a variable per-mile charge.

Exposure is captured through verified odometer reads, app-based mileage tracking, or telematics devices. That data continuously updates the insurer’s view of exposure, so premium is tied to actual miles driven, not a static annual mileage estimate provided at underwriting. The result is a pricing model that adjusts with real usage patterns, including seasonal shifts and changes in commuting behavior.

Best-Fit Customer Segments for Pay-As-You-Go Model

- Low-mileage drivers

- Remote and hybrid workers

- Retirees

- Urban residents with limited driving frequency

- Multi-vehicle households where one vehicle is rarely used

This segment has grown post-pandemic as commuting patterns remain structurally lower in many metropolitan markets.

Strategic Value for Insurers

Mileage-based models serve multiple strategic purposes:

- Defensive positioning against direct-to-consumer Insurtech competitors

- Retention tool for low-usage policyholders who might otherwise shop aggressively

- Data-rich entry point into broader telematics insurance programs

- Brand alignment with fairness-based pricing narratives

According to industry studies, drivers consistently cite “paying for unused mileage” as a top dissatisfaction driver in auto insurance. Mileage-based pricing addresses that perception gap directly.

For carriers with strong analytics capability, this model can improve risk segmentation without fully transitioning to behavior-based scoring.

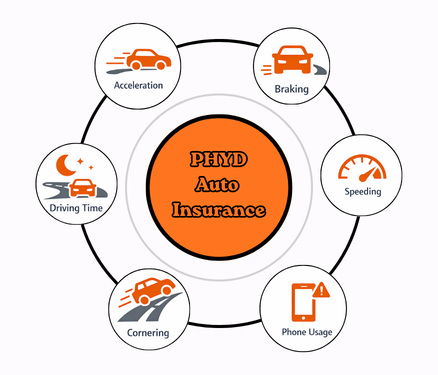

3. Pay How You Drive (Behavior-Based / Telematics Insurance)

Pay How You Drive is a form of telematics insurance where pricing is influenced not only by mileage, but by driving behavior. Data collected through mobile apps, plug-in devices, or embedded vehicle systems measures factors such as acceleration, braking, speed patterns, time of day, and in some programs, distraction indicators.

Unlike pure usage-based auto insurance models tied only to miles, this structure introduces behavior scoring into underwriting and pricing. Premium becomes partially dynamic, reflecting observed risk characteristics during the policy term.

Best-Fit Customer Segments for Pay How You Drive Model

- Younger drivers seeking discounts

- Safety-conscious households

- Parents monitoring teen drivers

- Digitally engaged policyholders

- Fleet-lite and gig drivers with trackable patterns

Behavior-based programs often attract customers who believe they are “better than average” drivers and want pricing that reflects that confidence.

Strategic Value for Insurers

Telematics insurance offers deeper strategic advantages than mileage-only models:

- Improved risk segmentation granularity

- More accurate frequency prediction models

- Early identification of deteriorating driving behavior

- Enhanced retention through engagement (driver score dashboards)

- Competitive differentiation in digital distribution

Industry research indicates that telematics-enabled policies can reduce claim frequency among participating drivers, particularly when feedback loops encourage safer driving behavior.

For insurers focused on underwriting accuracy rather than short-term pricing differentiation, this is a structural evolution. Behavioral data allows carriers to move beyond proxy variables and refine risk selection dynamically during the policy term. That can improve frequency forecasting, sharpen pricing adequacy, and reshape portfolio mix over time.

Related Read: Top 7 UBI Trends in the USA & How Auto Insurers Can Make the Shift

4. Subscription Auto Insurance

Subscription car insurance bundles auto coverage into a recurring monthly structure, often combined with vehicle access, maintenance, roadside assistance, or other mobility services. Instead of a fixed 6- or 12-month policy, coverage operates on a rolling subscription basis.

In some structures, insurance is embedded within a broader vehicle subscription. In others, the policy itself is structured as a month-to-month renewable agreement with simplified cancellation.

This model aligns insurance with subscription-based consumption patterns increasingly common across financial services and mobility ecosystems.

Best-Fit Customer Segments for Subscription Based Model

- Younger urban drivers

- Drivers using vehicle subscription platforms

- Customers seeking predictable monthly cost structures

- High-income convenience-focused consumers

- Households preferring bundled service models

This segment prioritizes simplicity and flexibility over long-term contractual commitment.

Strategic Value for Insurers

Subscription models create strategic opportunities beyond pricing:

- Integration into vehicle subscription ecosystems

- Increased customer engagement through bundled services

- Predictable recurring revenue flows

- Lower perceived commitment barriers at onboarding

- Potential cross-sell opportunities across mobility services

For carriers partnering with OEMs or mobility providers, subscription insurance becomes an embedded distribution play rather than a standalone product. The platform controls the purchase moment, bundles insurance into the monthly payment, and reduces shopping friction. That can improve conversion, but it also shifts economics around margin, data expectations, and channel leverage. In this setup, insurers win on underwriting performance, integration speed, and claims experience more than brand-led acquisition.

It also aligns with a broader shift toward recurring service relationships instead of fixed contracts. Customers increasingly expect one predictable monthly mobility bill, simple onboarding, and “change or cancel anytime” servicing. That raises the bar for billing accuracy, disclosure clarity, and near-real-time policy updates. Annual policy workflows often need modernization to deliver that experience consistently.

5. On-Off Insurance (Toggle Activation Model)

On-Off insurance allows policyholders to activate or deactivate certain coverage components, typically collision or comprehensive, through a mobile app or digital portal. The core liability coverage often remains active to comply with state minimum requirements, while optional coverages can be toggled.

The concept is simple: pay only when the vehicle is actively being used. However, from a regulatory and underwriting standpoint, it is more complex than it appears.

This model is often positioned as a form of on demand auto insurance, but structurally it is closer to controlled exposure modulation within an active policy.

Best-Fit Customer Segments for On-Off Insurance

- Seasonal drivers

- Owners of secondary or recreational vehicles

- Urban residents who park vehicles long-term

- Remote workers with irregular driving patterns

- Cost-sensitive policyholders seeking flexibility

This model resonates with drivers who view inactivity periods as “unused premium.”

Strategic Value for Insurers

On-Off insurance can serve as a retention tool in rate-sensitive markets.

Instead of losing a customer due to premium pressure, carriers offer controlled coverage reduction during low-usage periods. This can preserve the relationship while protecting core liability exposure.

It also signals responsiveness to consumer expectations around flexibility. However, its financial benefit depends heavily on how frequently customers toggle and how exposure truly shifts. If poorly designed, it can create premium leakage without meaningful risk reduction.

Quick Comparison Matrix of Six On-Demand Auto Insurance Models

| Model | Best-Fit Segment | Primary Pricing Basis | Fraud / Adverse Selection Risk | Channel Fit | Operational Complexity |

|---|---|---|---|---|---|

| Pay As You Need (Time-Based) | Occasional drivers, borrowed vehicle users, short-term access | Duration-based (hour/day/week) | High at bind; event-driven activation risk | Strong D2C; niche insurtech; non-owner distribution | High – requires real-time rating, instant issuance, fraud scoring |

| Pay As You Go (Mileage-Based) | Low-mileage, remote workers, retirees | Verified miles driven | Moderate – mileage manipulation risk | D2C; retention tool for existing book | Moderate to High – dynamic billing, mileage validation, disclosure control |

| Pay How You Drive (Telematics Insurance) | Younger drivers, safety-focused households | Behavioral scoring + usage data | Algorithm scrutiny; data governance exposure | D2C; agent-assisted with digital overlay | High – telematics ingestion, scoring engines, compliance oversight |

| Subscription Car Insurance | Urban, mobility-platform users, convenience-focused customers | Recurring monthly pricing | Churn volatility; pricing adequacy risk | OEM partnerships; vehicle subscription ecosystems | Moderate – recurring billing, rolling renewals, cancellation logic |

| On-Off Insurance | Seasonal or secondary vehicle owners | Toggle-based exposure modulation | Activation timing disputes; premium leakage | Primarily D2C mobile-first | High – real-time endorsements, audit trails, state compliance automation |

Risk and Compliance Considerations Before Launching Auto Insurance Product

On-demand auto insurance models introduce operational flexibility, but they also amplify compliance sensitivity. In the U.S., regulatory variation by state makes execution as important as product design.

Carriers evaluating temporary car insurance, usage-based auto insurance, telematics insurance, subscription car insurance, or embedded auto insurance must address several compliance dimensions early.

1. State Regulatory Variation

Auto insurance remains state-regulated.

Key considerations include:

- Minimum coverage duration requirements

- Financial responsibility laws

- Cancellation and non-renewal notice periods

- Filing requirements for telematics rating factors

- Restrictions on inducements in embedded sales models

Some states may limit how short a policy term can be. Others require explicit approval if telematics materially affects premium. Piloting in a limited number of aligned jurisdictions is often prudent before broader rollout.

2. Disclosure Clarity in Digital Journeys

On-demand structures are frequently sold through digital channels. That increases scrutiny around:

- Clear presentation of coverage limits

- Explanation of dynamic pricing components

- Toggle activation terms and conditions

- Renewal or subscription auto-renew logic

- Variable billing disclosures

Regulators increasingly evaluate whether consumers fully understand fluctuating premiums in mileage-based or telematics insurance programs. Ambiguity in digital UX can translate directly into complaint volume.

3. Proof of Insurance Timing

Real-time issuance creates compliance obligations.

Insurers must ensure:

- Instant generation of ID cards

- Timely reporting to state databases (where required)

- Clear timestamping of activation events (for On-Off models)

- Accurate lapse prevention controls

Coverage disputes around activation timing can quickly escalate into regulatory exposure if audit trails are weak.

4. Data Privacy and Telematics Governance

Behavior-based and mileage-based programs require careful data governance.

Considerations include:

- Customer consent protocols

- Data storage security

- Algorithm transparency

- State privacy laws (including emerging data protection statutes)

- Disparate impact analysis

Telematics data may be considered sensitive personal information depending on jurisdiction. Clear governance frameworks reduce both litigation and reputational risk.

5. Cooling-Off Periods and Refund Logic

Short-duration and subscription models raise questions about:

- Refund calculations

- Grace periods

- Mid-term premium adjustments

- Consumer rights in digital sales environments

States may require specific disclosures when coverage begins immediately at bind. Failure to align refund logic with state-specific rules can erode profitability and increase regulatory scrutiny.

Related Read: Questions Every Carrier Must Ask Before Launching a New Line of Business

Conclusion

On-demand auto insurance is not a replacement for the traditional annual policy. For carriers, it is a focused portfolio choice that can address specific customer needs, usage patterns, and growth opportunities more effectively. The value comes from matching the right model to the right objective: time-based cover as an acquisition tool, mileage-based and telematics models to improve pricing and segmentation, subscription models to support flexible vehicle access, and on-off activation to help retain low-usage customers.

The path forward should be targeted and practical. Carriers need to define the use case, choose the customer segment, pilot in a limited number of states, and validate loss performance before expanding. They also need to make sure their underwriting, compliance, billing, servicing, and data systems can support the model in practice.

This is where insurance strategic consultant such as Practo Insura can add value, helping carriers assess product-market fit, distribution strategy, risk appetite, and operational readiness before scaling. The insurers most likely to win will not be the ones that launch the most products. They will be the ones that choose carefully, execute well, and build the capability to scale with confidence as demand for more flexible auto insurance continues to grow.

We specialize in developing innovative Property & Casualty (P&C) insurance software solutions, leveraging over 8 years of InsurTech expertise to simplify insurance operations and enhance efficiency.

Share Article via

Subscribe to our insights newsletter

Related Blog Posts

Why Claims Data Matters in...

03 Jun, 2026

03 Jun, 2026

Claims data has traditionally been treated as a record of...

Read More

What Is Subscription Auto Insurance...

15 Apr, 2026

Auto insurance was designed for a market built on long-term...

Read More

What Is Pay How You Drive Auto...

03 Apr, 2026

Auto insurance pricing is already moving beyond fixed assumptions. Over...

Read More