Our Blog

Insurance Underwriting Automation: Implementation Guide for U.S. P&C Carriers and MGAs

12 Jun, 2026

12 Jun, 2026

Most P&C underwriters did not join the industry to chase MVR reports, re-key broker data into a policy administration system, or manually sort submission queues. Yet that is precisely where the majority of their day goes.

The work that actually demands underwriting judgment, risk assessment, pricing decisions, appetite exceptions, portfolio analysis, often sits buried beneath layers of administrative process that have never been redesigned. The result: slower quote turnaround, rising operational costs, and experienced underwriters spending most of their time on tasks a well-configured system could handle automatically.

Insurance underwriting automation is built to fix that. But here is the reality most guides skip: only about 35% of automation initiatives meet their stated goals, according to BCG's analysis of 850 companies. The failure rate is not a technology problem. It is an architecture, data quality, and integration problem, and this guide addresses all three.

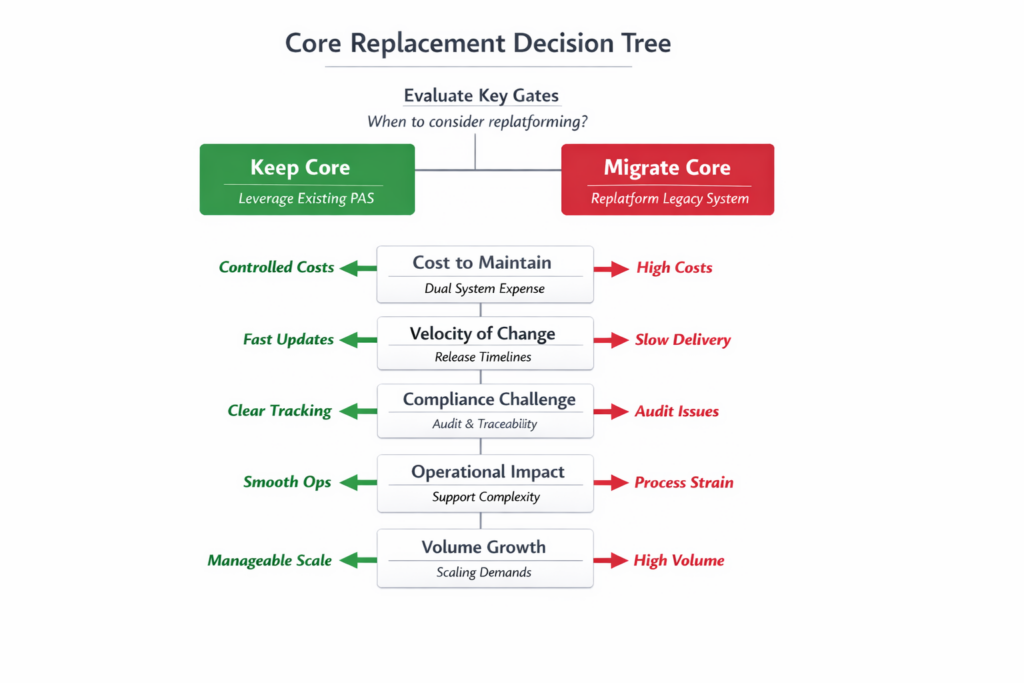

What Underwriting Automation Actually Means in 2026

Underwriting automation is not a single product. It is a spectrum of capabilities, and where your organization sits on that spectrum determines where you should start.

At one end: a basic rules engine that auto-approves clean, low-risk submissions based on pre-defined criteria; no ML, no AI, just structured logic. At the other: an agentic underwriting system that ingests submissions in any format, enriches data from external sources in real time, scores risk against your appetite, and routes decisions automatically from submission to bind.

Most mid-market P&C carriers and MGAs sit closer to the left side of that spectrum. Many are still relying on underwriters to manually pull motor vehicle records, re-enter broker PDFs into their PAS, and prioritise their own queues. Automation closes those gaps first, not by replacing underwriters, but by removing the work that should never have required them.

Underwriting automation means removing manual touchpoints from the submission-to-bind workflow so that underwriters spend their time on risk judgment, not data processing.

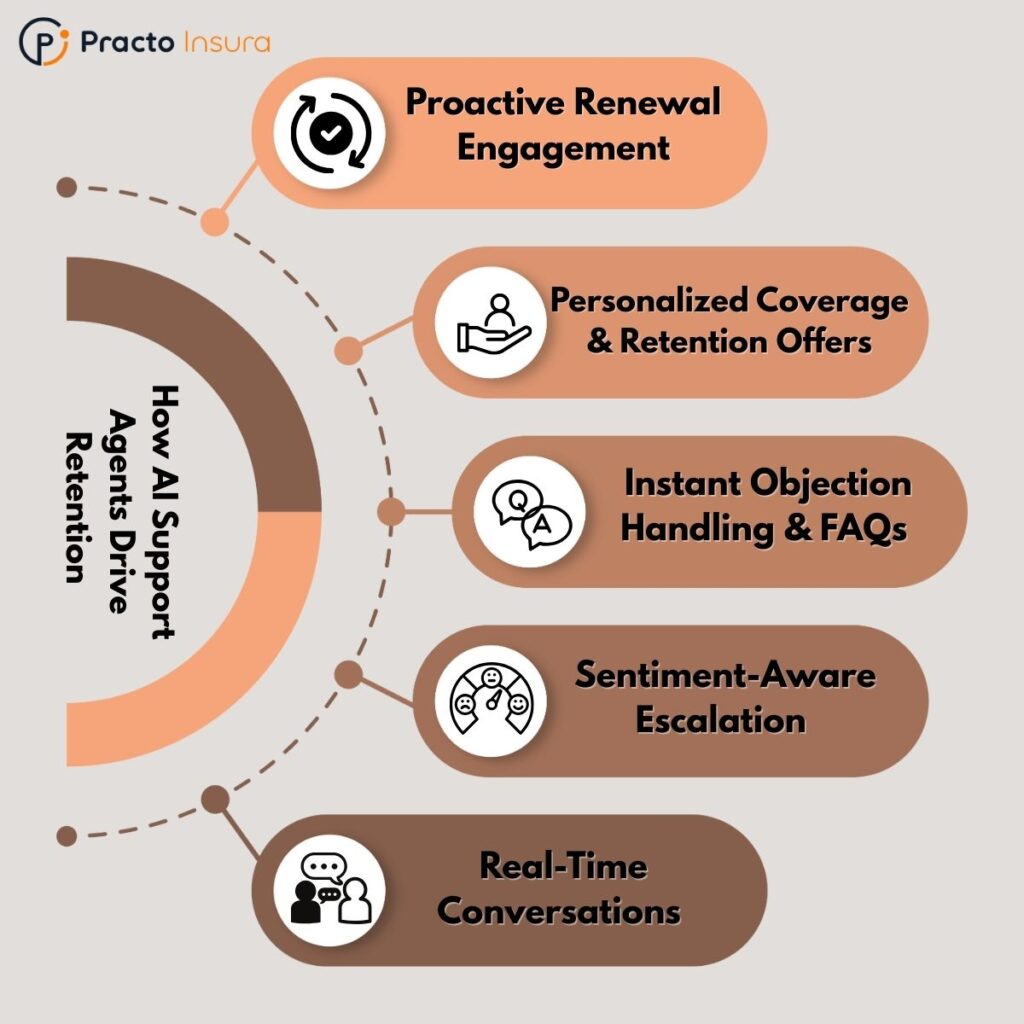

5 Underwriting Workflows to Automate First Prioritized by ROI

Most carriers ask the same question when they start: where do we begin? The answer is not "everywhere at once." Below are the five workflows ranked by ROI potential and implementation difficulty, based on patterns seen across mid-market automation projects.

1. Submission Triage and Routing

Commercial lines underwriting teams face a structural imbalance: they receive far more submissions than they can evaluate thoroughly, and the volume is growing. Submissions arrive in inconsistent formats: PDFs, emails, ACORD forms, broker portals and someone has to read, classify, and route each one.

Automating triage means the system reads each incoming submission and extracts the key risk attributes, automatically, the moment it arrives.

It then scores the submission against your underwriting appetite criteria and routes it in seconds. No human touchpoint required.

The routing logic is straightforward:

- Clean, in-appetite risks go straight through to bind

- Complex cases go to the referral queue with context already assembled

- Out-of-appetite submissions are declined automatically

In commercial lines, this single workflow typically saves 20–30 minutes per submission. At volume, that is significant underwriter capacity recovered every week — without adding headcount.

STP benchmarks by line of business:

| Line | Achievable STP rate | Notes |

|---|---|---|

| Personal auto | 80–90% | Clean data sources; well-defined rules |

| Homeowners (non-CAT exposed) | 70–85% | Higher in standard territories |

| Simple BOP / small commercial | 60–75% | Depends on data completeness |

| Commercial auto | 40–60% | MVR complexity limits STP ceiling |

| Specialty / E&S lines | 15–35% | Risk complexity requires human judgment |

Benchmarks sourced from ScienceSoft's 2026 underwriting automation research and industry practitioner data.

2. AI Document Processing for Submission Intake

Manual data extraction, reading broker PDFs, pulling figures from loss runs, re-keying ACORD forms into the PAS, is where underwriters lose hours every day. None of that work requires underwriting judgment. It requires reading comprehension and data transfer, which NLP and OCR handle accurately at any volume.

A mid-market personal and commercial auto carrier automating submission intake, before touching any decision logic, has documented quote turnaround reductions from three to five business days down to under four hours. The change is not a new underwriting model. It is removing the manual data re-entry step between broker submission and underwriter review, a result consistent with McKinsey's finding that workflow redesign not the AI tool itself is the single strongest driver of operational improvement.

This workflow is particularly high-value for commercial lines MGAs that receive heterogeneous broker submissions at high volume and must feed structured data into carrier reporting systems.

3. Rules-Based STP for Clean Risks

For personal lines and simple small-commercial submissions that meet your clean-risk criteria, there is no analytical reason for a human to review every file. A well-configured rules engine can handle the full submission-to-bind workflow, data check, eligibility verification, rating, and issuance, without human intervention.

ScienceSoft's research shows that best-in-class automation achieves application processing in under four minutes for standard policies, compared to days or weeks in manual workflows. That speed advantage compounds: faster binding improves broker relationships, reduces quote-to-close abandonment, and lets underwriters concentrate on the complex submissions that genuinely need their judgment.

A personal lines auto carrier starting from under 20% STP pre-automation and reaching 80% STP on standard private passenger submissions after 90 days of rules refinement is a documented outcome consistent with Capgemini's finding that underwriting trailblazers, the top 8% of P&C insurers achieve STP rates in the 70-90% range for standard personal lines. The consistent differentiator is iterating on rules weekly during the first quarter, not configuring once and stepping back.

4. Renewal Pre-Fill and Risk Re-Scoring

Renewal underwriting is frequently more manual than new business despite being lower risk. Underwriters re-pull data, re-check flags, and review accounts that have not materially changed in 12 months. For a mid-size carrier renewing 50,000 policies annually, that represents enormous low-value volume.

Automating renewal workflows means the system pulls updated third-party data before the renewal date, re-scores each account against current appetite criteria, flags accounts with material changes for human review, and pre-fills renewal documents for accounts that pass. This workflow also drives measurable retention improvement: when the system identifies at-risk renewals early, outreach can happen proactively rather than reactively.

A specialty MGA automating renewal pre-fill for a contractors' liability book, pulling updated loss data, re-scoring against appetite, and pre-filling renewal documents, can reduce renewal processing time by 50–65% within the first two quarters, an outcome consistent with BCG's finding that carriers implementing end-to-end AI redesign achieve materially better outcomes than those adding automation to unchanged processes.

5. Referral Queue Management andPrioritization

Even with STP in place for clean risks, complex submissions still require human review. The question is whether underwriters spend time deciding what to work on, or actually working on it.

Automated queue management scores each referred submission by priority, premium size, risk complexity, relationship value, time sensitivity assembles the data package the underwriter needs before they open the file, and routes it based on line of business expertise. The underwriter opens a submission with external data already pulled, appetite criteria already checked, and a risk summary already assembled.

This workflow does not reduce the number of referred submissions. It reduces the administrative overhead of each one, typically by 15–25 minutes per referral.

Why Mid-Market Carriers and MGAs Face Particular Pressure

Three forces are converging in 2026 that make automation a financial necessity rather than a technology aspiration for mid-market operators specifically.

- Combined ratios are deteriorating after the hard market plateau.

The industry-wide combined ratio is forecast to worsen from 97.2% in 2024 to 99% by 2026, according to Deloitte's 2026 Insurance Outlook. Carriers that relied on four years of rate increases to offset operational inefficiency no longer have that buffer. The next margin lever is expense ratio improvement, and manual underwriting processes are one of the largest controllable cost items. - Experienced underwriters are retiring, taking institutional knowledge with them.

McKinsey's Global Insurance Report 2025 found that leading insurers are nearly twice as likely to have prioritized significant technology investment in underwriting operations compared to bottom-quartile performers. The carriers investing now are capturing appetite rules, exception logic, and risk intuition in systems before it walks out the door. - The competitive gap is widening rapidly

McKinsey's Global Insurance Report 2025 also notes that leading insurers achieve loss ratios six percentage points better than competitors, and that operational strategies account for 60% of overall insurer performance. In a softening market where speed to quote determines whether a carrier wins or loses business, the administrative overhead of manual underwriting is a direct competitive disadvantage.

The Automation Technology Stack: Choosing the Right Tool for Each Workflow

One of the most common mistakes carriers make is treating "underwriting automation" as a single technology decision. It is not. Different workflows require different tools, and the wrong match is one of the leading causes of underperforming implementations.

| Technology | Best suited for | Why |

|---|---|---|

| Rules engine | Personal lines, simple BOP, high-volume standard risks | Deterministic, auditable, fast to configure. Ideal for STP where criteria are binary and well-defined. |

| AI document processing (NLP/OCR) | Commercial lines submission intake, loss run analysis | Reads unstructured submissions in any format, extracts data, reduces manual re-keying. |

| ML risk scoring models | Complex commercial, specialty, E&S lines | Identifies non-linear risk signals across hundreds of variables that rules engines miss. |

| Workflow automation / BPM | Referral routing, renewal workflows, queue management | Orchestrates tasks across teams and systems without requiring AI decision-making. |

| Agentic AI | High-complexity submissions requiring multi-step reasoning | Handles entire intake-to-decision workflows autonomously; requires the most governance. |

Most mid-market carriers should not begin with fully autonomous underwriting. A more practical path is to start with a rules engine for high-volume personal lines or simple small commercial risks, then add AI document processing to automate submission intake. ML-based risk scoring should come later, once data quality has been validated. More advanced capabilities, such as agentic AI and full underwriting workbench deployments, are usually better suited for later phases after the core workflow and integration layer are stable.

Why Most Underwriting Automation Projects Underperform

BCG’s 2025 global study of 1,250 companies found that only 35% of transformation initiatives meet their stated goals. In underwriting automation, the failure pattern is usually not the AI model itself. It is poor data quality, weak integration, broken workflows, and missing governance.

Failure point 1: Data quality is treated as an afterthought.

The Capgemini World P&C Insurance Report 2024 found that 70% of insurers cite inconsistent underwriting decisions as a prevailing issue, largely driven by data quality and governance challenges. Inconsistent formats, missing fields, duplicate records, and fragmented legacy data mean automation can produce fast, wrong decisions. Successful carriers clean and validate their data before configuring automation logic.

Failure point 2: Automation is layered onto broken workflows.

McKinsey’s 2025 State of AI report found that high-performing organizations are nearly three times more likely to redesign workflows around AI rather than simply add AI to existing processes. If a manual, approval-heavy workflow is automated without redesign, the result is only a faster version of the same inefficient process.

Failure point 3: PAS integration is underestimated.

BCG’s 2026 Executive Perspectives on P&C Insurance found that 35% of insurance applications still run on legacy technology stacks that are not cloud-ready. When the automation layer cannot communicate with the PAS, rater, or policy issuance module, the workflow breaks at the final step and manual work returns. Leading carriers test PAS integration early, not after decision logic is already configured.

Failure point 4: Governance is added too late.

KPMG’s 2025 analysis of technology implementation failures cites poor data governance and unclear requirements as common failure drivers. In underwriting automation, that means undocumented rules, no bias-testing process, and no defined escalation path for edge cases. Carriers that document rules, assign ownership, and define human-review criteria before go-live reduce compliance and rollback risk.

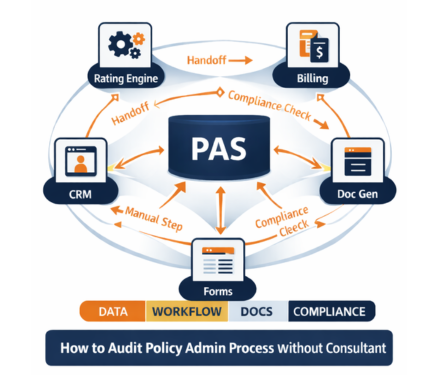

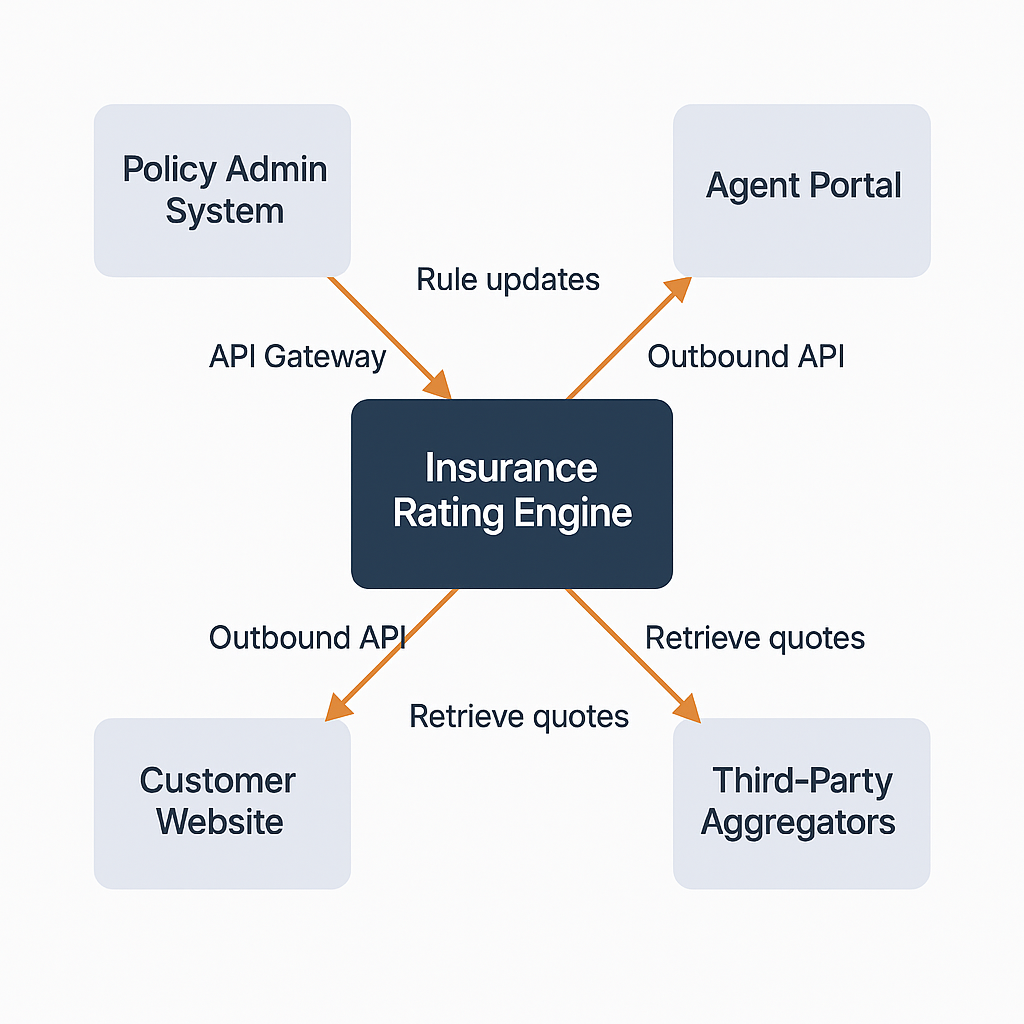

How Automation Connects to Your PAS and Rater Engine: The Integration Layer Most Carriers Miss

Underwriting automation that cannot talk to your policy administration system delivers half the value at full cost. The integration requirement is specific:

- Your rater must receive dynamic inputs from the automation layer.

If the rules engine approves a risk but your rating engine requires manual data re-entry to price it, you have automated the decision but not the workflow. The data captured at submission should flow forward to the rater without human intervention. - Your PAS must act on automated decisions.

When the rules engine approves a clean-risk submission, the PAS should issue the policy automatically via API. This requires deliberate integration work, it does not happen by default. - A single data capture at submission must feed every downstream system.

Bordereaux reporting, carrier data feeds, compliance documentation, and billing all need accurate data from the same submission record. Every additional re-entry point introduces error and compliance risk.

Carriers operating on cloud-native, API-first PAS platforms have a structural advantage here. The right core tech stack is a prerequisite to automation at scale, not something to address after implementation. Legacy PAS platforms often require significant middleware development to achieve the same data flow, which is worth planning for in the project budget before vendor selection.

For MGAs, the integration requirement extends to carrier partner systems. Your automation must produce the data formats, bordereaux structures, and reporting outputs your carriers contractually require. An automation layer that operates as a silo from your MGA management system creates reconciliation work that erodes the efficiency you built.

Related Read: How to Build Right Core Technology Stack for P&C Insurer

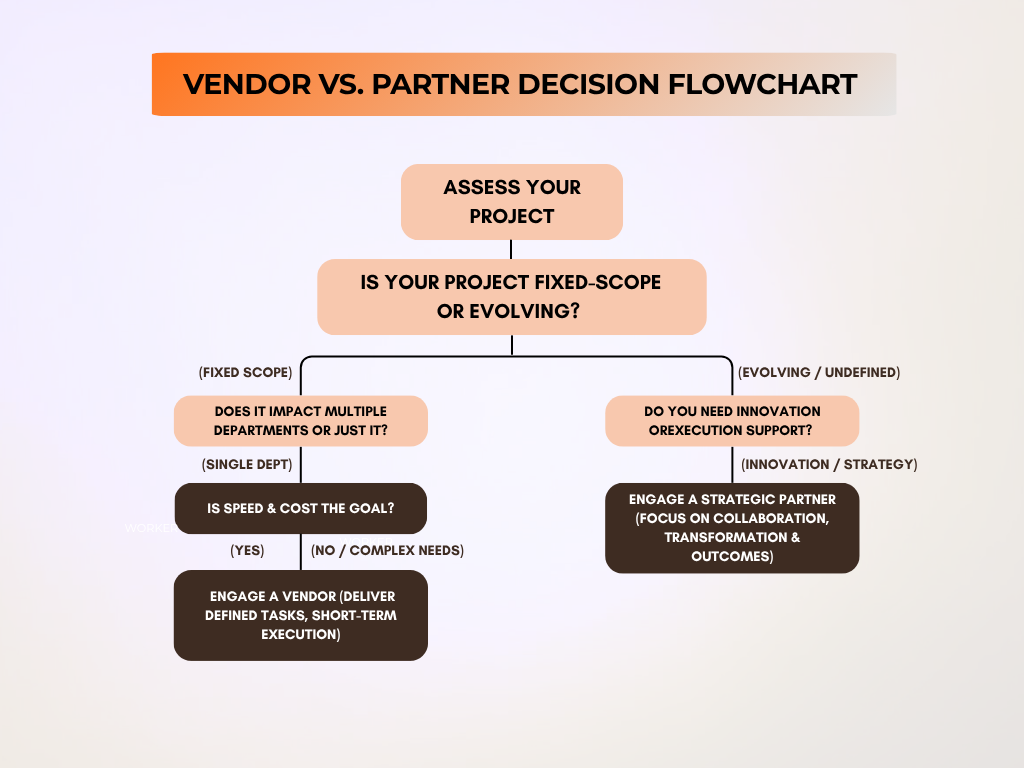

Build vs Buy: How to Choose the Right Approach for Your Organization

Every carrier and MGA evaluating underwriting automation eventually hits the same fork in the road: do we build this internally, buy a platform, or configure a pre-built solution? There is no universal answer, but there is a framework for making the right call based on your size, technical maturity, and competitive priorities.

The four options, and who each suits

Option 1: Build internally

You develop the rules engine, data integrations, and workflow logic using internal engineering resources or contract developers.

Best for: Large carriers ($1B+ GWP) with dedicated engineering teams, a proprietary risk model that is genuinely differentiated, and a multi-year runway for development and maintenance.

Reality for mid-market: Most mid-market carriers do not have the engineering capacity to build, maintain, and iterate on an underwriting automation system while also running daily operations. McKinsey's research shows companies that redesign workflows end-to-end achieve 3× better AI outcomes than those that treat it as a technology project, and that redesign work competes directly with build capacity.

Option 2: Buy a standalone automation platform

You purchase a dedicated underwriting workbench or automation tool and integrate it with your existing PAS and rater.

Best for: Carriers with a functioning PAS that has open APIs and a reasonably clean data layer. Works well when the existing core system is sound and only the underwriting workflow layer needs upgrading.

Watch for: Integration cost is frequently underestimated. BCG's 2026 P&C Executive Perspectives found that 35% of insurance applications still run on legacy stacks that are not cloud-ready, buying a modern automation tool and connecting it to a legacy PAS often requires more middleware development than the tool itself costs.

Option 3: Buy + configure (SaaS with configurable rules)

You deploy a pre-built underwriting automation platform where the rules engine, workflow logic, and data integrations are configurable by your underwriting and product teams, without requiring developer involvement for routine changes.

Best for: Mid-market carriers and MGAs that need to be live in months, not years, and want underwriting and product staff to own the rules without IT dependency. A no-code and low-code configuration is particularly valuable for MGAs managing high volumes of products across multiple lines who need to respond to market opportunities quickly.

This is the most common starting point for $100M–$500M GWP carriers and growing MGAs.

Option 4: Modern PAS with native automation capabilities

Rather than adding a separate automation tool on top of your existing core system, you move to a PAS that includes built-in rules engine, rater integration, workflow orchestration, and bordereaux generation with automation as a native capability rather than a bolt-on.

Best for: Carriers and MGAs that are also evaluating a PAS upgrade or replacement. If your current PAS is a barrier to integration, solving the PAS problem and the automation problem simultaneously is significantly more cost-effective than solving them sequentially.

The decision framework

Ask these four questions before choosing a path:

| Question | Build Internally | Buy Standalone | Buy + Configure | PAS-Native Automation |

|---|---|---|---|---|

| Do you have a dedicated engineering team? | Required | Helpful | Not required | Not required |

| Is your current PAS API-ready? | Helpful | Required | Helpful | Not required |

| Do you need to launch within 12 months? | Rarely realistic | Possible | Likely | Likely |

| Is your underwriting logic highly proprietary? | Best fit | Moderate fit | Moderate fit | Lower fit |

| Do business users need to update rules without IT? | Difficult | Depends on vendor | Yes | Yes |

| Is your current PAS already a constraint? | Does not solve it | Does not solve it | Partially solves it | Best fit |

| Best suited for | Large carriers with strong engineering teams | Carriers with modern API-ready cores | Mid-market carriers and MGAs | Carriers or MGAs replacing legacy PAS |

What Does Underwriting Automation Cost? A Budget Framework for 2026

Cost is the question most guides avoid answering. The honest answer is that investment ranges vary significantly based on organization type, build-vs-buy decision, and scope of the first phase.

The table below provides indicative budget guidance based on observed SaaS and configure-and-deploy market pricing. These are directional estimates, not quoted prices, actual costs depend on vendor, scope, data complexity, and legacy integration requirements. Use them for initial scoping conversations, not final budgeting.

| Organisation type | Typical Phase 1 investment (U.S.) | What it typically covers |

|---|---|---|

| Small MGA (under $50M GWP) | $50,000–$150,000 | SaaS rules engine, submission intake automation, and limited integration work for a single line of business |

| Mid-market MGA ($50M–$200M GWP) | $150,000–$500,000 | Configurable underwriting automation, STP workflows, renewal automation, and PAS/rater integration |

| Regional carrier ($200M–$500M GWP) | $500,000–$1.5M | Underwriting workbench, PAS integration, data validation layer, and rollout across multiple lines |

| Mid-size carrier ($500M–$1B+ GWP) | $1M–$5M+ | Enterprise implementation including legacy system integration, workflow redesign, governance controls, compliance requirements, and multi-line deployment |

Where budget typically goes in a Phase 1 project (indicative estimates based on practitioner experience, actual allocation varies by project):

- Licensing / platform fees: 30-45% in SaaS deployments; the smallest component in custom builds

- Integration and data work: 35–50% in connecting to existing PAS, MVR providers, and carrier reporting systems is consistently the most underestimated line item

- Rules configuration and testing: 10–20% in documenting, building, and validating appetite rules before go-live

- Compliance and governance setup: 5–10% in audit trail design, bias testing protocol, NAIC documentation

The hidden cost most budgets miss: data quality remediation. If your existing PAS data has inconsistencies, duplicate records, non-standardised fields, legacy migration artefacts, cleaning it before automation go-live typically adds meaningful unplanned cost.

ROI timeline: A 12–18 month payback period for underwriting automation is a commonly cited industry benchmark, driven primarily by underwriter capacity reallocation and improved broker hit rates from faster quote turnaround. Independently verified ROI timelines for underwriting automation specifically are not widely published, so treat this as a directional range rather than a guarantee.

How to Get Started: A 4-Step Incremental Approach

The most common mistake mid-market carriers make is treating underwriting automation as an all-or-nothing transformation. The second most common mistake is waiting for perfect data before starting. Neither works.

Step 1: Audit one high-volume, low-complexity line

Select a single line of business, personal auto, homeowners, or simple BOP, where submission volume is high, risk criteria are well-defined, and your appetite rules are already documented in some form. This becomes your automation pilot. Do not start with commercial casualty or specialty lines.

Step 2: Clean data and automate triage and intake for that line only

Before touching any decision logic, address data quality for your pilot line and implement automated submission intake and third-party data pulls. This step alone recovers significant underwriter time and validates your data foundation before automated decisions are made on top of it.

Step 3: Implement STP connected to your rater and iterate weekly

Configure rules-based auto-approval for clean-risk submissions in your pilot line. Critically, confirm the integration to your PAS and rater before go-live so that approved submissions issue automatically. Monitor results weekly for the first 90 days. Adjust rules as you observe the submission population. STP rates improve meaningfully with iteration in the first quarter.

Step 4: Expand to renewal workflows and additional lines

Once one line is operating with reliable STP, clean data flows, and a functioning audit trail, expansion to renewal pre-fill and additional lines follows the same pattern. Each line benefits from the infrastructure and governance framework built in Steps 1–3.

This approach takes 6–12 months to reach meaningful scale for a mid-market carrier or MGA. It is slower than a full-platform replacement and significantly lower risk, and the carriers that follow it have materially better outcomes than those who attempt to automate everything at once.

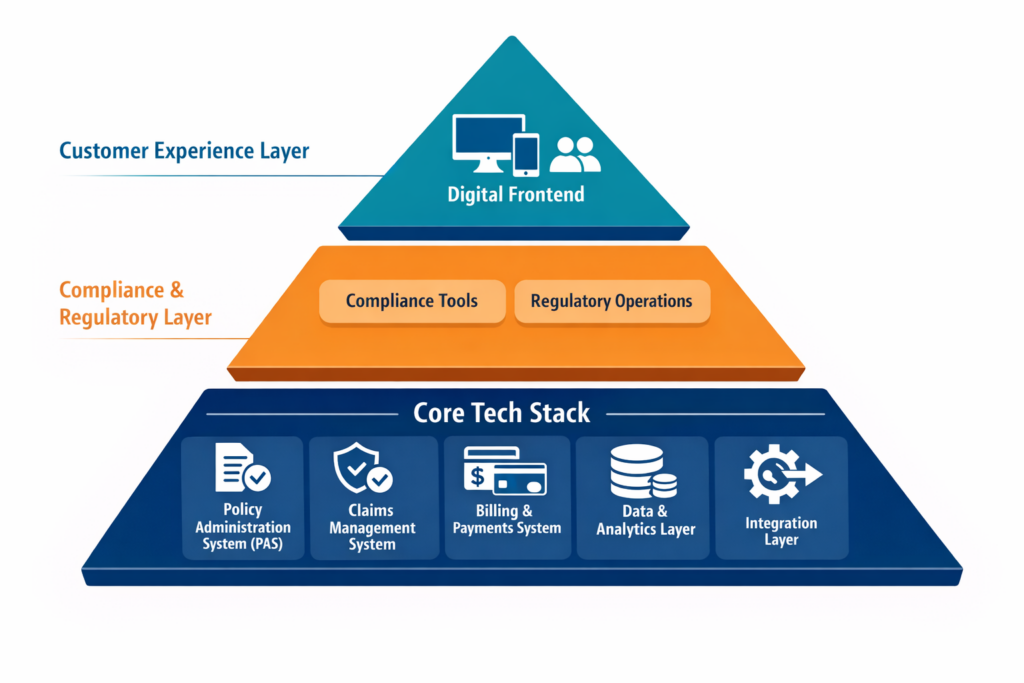

Is Your PAS Ready for Automation?

The sections above converge on the same practical question: does your current policy administration system satisfy the four integration requirements that underwriting automation depends on?

Specifically: does it expose real-time APIs, accept dynamic rater inputs, generate bordereaux natively, and include a workflow orchestration layer, without requiring a middleware project to connect each piece?

If the answer is no, the most cost-effective path is often to solve the PAS problem and the automation problem together rather than sequentially. Retrofitting automation onto a PAS that was not designed for it is one of the most common sources of project overrun in mid-market underwriting technology programmes.

Practo Insura's policy administration system is built with these four requirements as native capabilities: an API-first architecture, a built-in Rapid Rater engine, real-time MVR and third-party data integration, and workflow orchestration for referral routing and compliance escalation, designed specifically for mid-size U.S. P&C carriers and MGAs.

If you are evaluating whether your current PAS can support your automation roadmap, request a demo to see how the platform connects to your existing systems and what a phased automation implementation would look like for your lines of business.

Why Claims Data Matters in Product Design for U.S. P&C Insurer

03 Jun, 2026

Claims data has traditionally been treated as a record of past losses, used mainly for reserving, reporting, and post-event analysis. But in today's U.S. P&C market, where repair severity, litigation exposure, climate volatility, and emerging risks are changing faster than traditional product cycles, claims data is becoming a strategic input for product design, pricing, and underwriting decisions.

The real challenge is no longer whether insurers have claims data, every carrier does. The challenge is how quickly they can convert claims signals into business action. As the gap between changing risk conditions and organizational response widens, claims intelligence is becoming a critical capability for improving underwriting performance, product relevance, and long-term profitability.

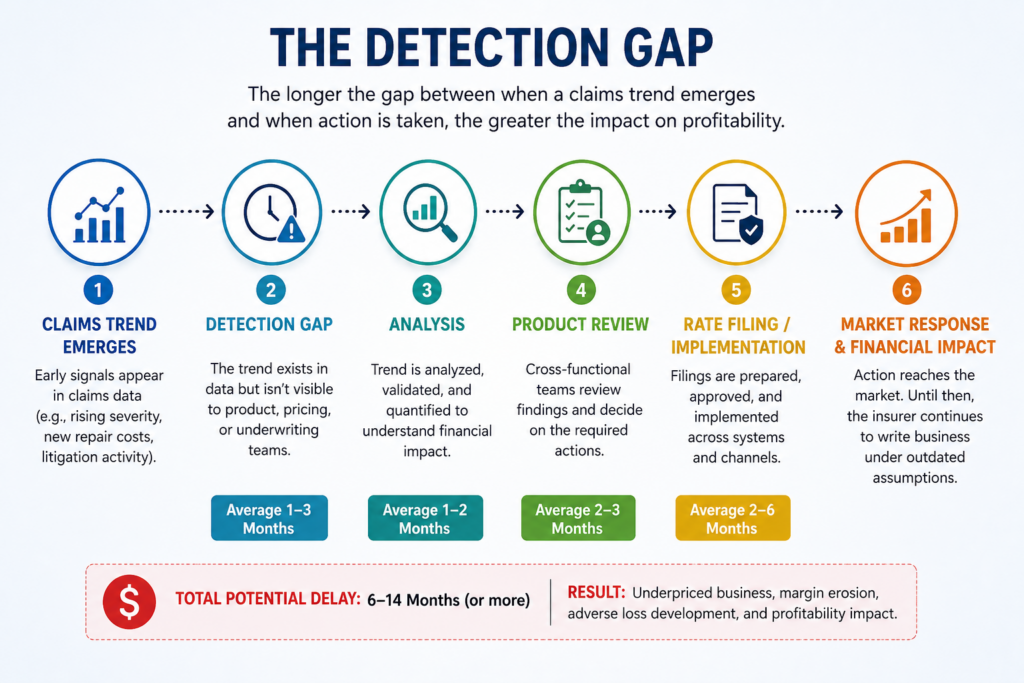

What is Detection Gap in Modern Insurance Product Design

Most carriers do not struggle because they lack claims data. They struggle because there is often a significant gap between when a claims trend emerges and when the organization takes action.

Consider a common auto insurance example. Claims teams may start seeing higher repair severity for specific vehicle segments due to increasing ADAS calibration requirements, longer repair cycles, or more expensive replacement parts. The signal exists. The data exists. The problem is that product, underwriting, and pricing teams may not see that trend until months later through formal reviews or profitability reporting.

That delay creates what can be called the Detection Gap, the period between when claims data first signals a meaningful change in risk and when the organization responds with a pricing, underwriting, or product adjustment.

Why the Detection Gap Matters

The financial impact of a claims trend is rarely immediate. Instead, it accumulates quietly across hundreds or thousands of policies before it becomes visible in portfolio-level metrics.

- A severity trend may emerge today.

- A product team may detect it three months later.

- Analysis and validation may take another two months.

- A rate filing may require several more months before implementation.

By the time corrective action reaches the market, an insurer may have spent nearly a year writing business under assumptions that no longer reflect actual risk conditions.

The challenge is not limited to auto insurance. Similar detection gaps appear across P&C lines through:

- emerging weather-related loss patterns

- litigation-driven bodily injury severity

- coverage disputes and claims escalation trends

- organized fraud activity

- geographic concentration risk

In many cases, claims activity identifies these issues long before they appear in underwriting profitability reports.

From Claims Data to Business Action

Closing the detection gap requires insurers to think differently about claims information.

Claims data alone has limited value. What matters is how quickly that data becomes actionable intelligence.

The progression looks like this:

Claims Data → Pattern Detection → Business Decision → Product Action

The faster an organization moves through this cycle, the faster it can:

- adjust pricing assumptions

- refine underwriting appetite

- redesign coverage structures

- manage emerging risks

- protect portfolio profitability

This is why leading insurers increasingly treat claims intelligence as a strategic product management capability rather than a claims reporting function.

Why Claims Data Has Become a Strategic Product Asset

Claims data was once treated mainly as an operational record: what happened, what was paid, and how claims were handled. But for modern P&C insurers, that view is too limited.

Every product decision eventually shows up in claims. Pricing decisions affect profitability. Underwriting rules affect loss frequency. Coverage wording affects disputes. Deductibles affect claim behavior. Geographic expansion affects concentration risk.

That is why claims data has become a strategic product asset. It helps insurers validate whether product assumptions still match real-world risk conditions before problems appear in high-level profitability reports.

For carriers, MGAs, and reinsurers, the value is not simply having more claims data. The value is converting claims signals into faster pricing, underwriting, coverage, and portfolio decisions.

1. Validating Pricing and Underwriting Decisions

Pricing and underwriting decisions are built on assumptions. Claims data is where those assumptions are tested against actual loss behavior.

A rate plan may assume that a certain vehicle class, territory, driver profile, or coverage type carries a predictable level of risk. But once claims begin developing, insurers can see whether that assumption still holds. This is especially important in auto insurance, where repair severity, bodily injury trends, litigation involvement, and vehicle technology can change the economics of a segment quickly.

The impact is already visible in repair data. According to industry research, the average total cost of repair has increased 96.4% since 2009, rising from approximately $2,405 to more than $4,720 in 2024. Nearly half of that increase occurred within the last five years alone. ADAS-related costs are a major contributor. Calibration fees increased from $168 in 2017 to $488 in 2024, while diagnostic-related costs per 100 claims grew from roughly $580 to more than $21,300.

At the same time, auto insurance claims have increased 14% since 2020, while claims severity has risen 36%. For product and underwriting teams, these trends demonstrate how quickly actual loss costs can diverge from historical pricing assumptions.

What Claims Data Helps Validate

Claims data can show whether:

- certain vehicle types are producing higher severity than expected

- specific territories are generating more frequent or more expensive claims

- bodily injury trends are worsening in particular states

- deductible structures still make sense for current repair costs

- underwriting rules are attracting the right risk profile

- rating variables are still aligned with actual loss outcomes

For example, if newer vehicles with advanced safety systems are consistently producing higher repair costs than expected, the issue is not just claims severity. It may indicate that the current pricing model, deductible design, or underwriting assumptions need to be refined.

What Insurers Can Do With This Insight

Product and underwriting teams can use claims intelligence to make targeted changes, such as:

- revising rating factors

- adjusting deductible options

- tightening eligibility rules

- updating underwriting guidelines

- modifying territory assumptions

- flagging specific segments for pricing review

- redesigning coverage structures where loss behavior has changed

This prevents claims insight from staying trapped inside claims operations. It turns the data into a practical input for product and underwriting decisions.

The Result

When insurers use claims data to validate pricing and underwriting assumptions, they gain a clearer view of where the product is still working and where it is drifting away from real risk.

The result is sharper segmentation, better risk selection, stronger rate adequacy, and more disciplined portfolio management.

Related Read: How Insurers Use Predictive Analytics to Improve Underwriting and Risk

2. IdentifyingCoverage Gaps and Emerging Risks

Claims activity often reveals a different kind of product problem: not whether the price is right, but whether the coverage itself still works in the real world.

A product may be priced correctly and still create friction if policy wording is unclear, endorsements are outdated, limits no longer reflect current costs, or new exposures were not considered when the product was designed. These issues usually surface during claims, when customers test the product under actual loss conditions.

What Claims Data Reveals

Claims data can show:

- which coverages generate the most disputes

- where policy language creates confusion

- which endorsements are producing unexpected loss behavior

- whether limits or deductibles still match current repair and replacement costs

- where new risks, such as EV repairs, severe weather, or litigation trends, are creating product pressure

For example, an auto insurer may find that rental reimbursement limits are no longer adequate because repair cycle times have increased. A property insurer may see repeated disputes around water damage or storm-related exclusions. An MGA may discover that a niche endorsement is being used differently than originally expected.

What Insurers Can Do With This Insight

Product teams should treat these patterns as design feedback, not just claims friction.

That means insurers can:

- review dispute trends by coverage type

- analyze escalation patterns tied to specific policy wording

- reassess limits, deductibles, and exclusions against current claim realities

- update endorsements where loss behavior has changed

- involve claims and compliance teams before product changes are finalized

The Result

Using claims data this way helps insurers close coverage gaps before they become larger profitability, litigation, or customer experience problems.

It also makes product design more grounded in real claim behavior, not just market assumptions, competitor forms, or historical coverage structures.

3. Reducing Fraud and Claims Leakage

Fraud is not always obvious at the individual claim level. One inflated repair supplement, one represented injury claim, or one unusual billing pattern may look isolated. The real signal appears when similar patterns repeat across vendors, geographies, coverages, or claim types.

That is where claims intelligence becomes valuable. It helps insurers move beyond claim-by-claim review and identify leakage patterns that point to broader product or process vulnerabilities.

A 2024 study by CLARA Analytics found that AI-driven cohort modeling identified potential fraud indicators within two weeks of claim submission. Approximately 9% of open claims were flagged as strong SIU referral candidates, with the model identifying suspicious activity at a rate comparable to experienced adjusters but significantly earlier in the claim lifecycle.

Where Leakage Often Shows Up

Common signals include:

- repeated supplement requests from specific repair vendors

- abnormal medical billing patterns

- recurring use of the same coverage provisions

- staged accident indicators

- unusual claim timing or clustering

- claim types with higher-than-expected escalation rates

For example, if a specific endorsement is repeatedly involved in questionable claims, the issue may not be limited to fraud investigation. The endorsement itself may need clearer eligibility rules, stronger documentation requirements, or tighter claim controls.

How Insurers Can Respond

Insurers can reduce leakage by:

- standardizing vendor and provider tracking

- connecting SIU findings with product and underwriting teams

- reviewing claim pathways that are repeatedly exploited

- tightening documentation requirements where abuse patterns appear

- monitoring fraud indicators by coverage, vendor, geography, and claim type

Result

This helps insurers reduce avoidable claim costs while improving product discipline.

More importantly, it turns fraud detection into a product feedback mechanism. If claims data shows where the product is being exploited, insurers can redesign the exposure instead of only investigating it after the loss occurs.

Related Read: 5 Questions Every Carrier Must Ask Before Launching a New Line of Business

4. Improving Product Profitability and Portfolio Performance

Growth can hide weakness in a P&C portfolio. A product may continue adding premium while certain geographies, coverages, or customer segments quietly produce more volatility than expected.

Claims intelligence helps insurers separate healthy growth from fragile growth.

According to AM Best, the P&C industry's combined ratio improved from 101.6 in 2023 to 96.6 in 2024, driven in part by stronger pricing discipline, improved underwriting performance, and broader use of analytics.

Where Portfolio Pressure Often Appears

Claims data can reveal:

- geographies with concentrated or worsening loss activity

- coverages creating unexpected volatility

- segments requiring stronger reserve attention

- claim types affecting reinsurance confidence

- products where growth is outpacing risk control

- business classes producing unstable loss development

For example, a carrier may expand successfully in written premium, but claims activity may show that one region is becoming more exposed to weather losses or litigation-heavy claim behavior. That does not always mean the product should exit the market. It may mean the insurer needs tighter appetite rules, different deductibles, revised limits, or a different reinsurance view.

How Insurers Can Respond

Product, underwriting, and portfolio teams can use claims intelligence to:

- identify where growth should be accelerated, slowed, or restricted

- evaluate product performance below the portfolio-average level

- reassess limits, deductibles, and appetite by region or segment

- use claim volatility trends in reinsurance planning

- decide whether certain products need redesign before expansion continues

Result

Claims-informed portfolio management helps insurers grow with more discipline.

It gives leadership a clearer view of which parts of the portfolio are sustainable, which require correction, and which may create future volatility if left unmanaged.

5. Accelerating Product Innovation and Customer Experience Improvements

Product innovation does not always start with a new idea. Sometimes it starts with repeated claims patterns that show where customers need better protection, clearer service, or a product built for newer risk behavior.

Claims data gives insurers a practical view of how products perform after purchase, when the policyholder actually needs the coverage.

In 2024, more than 21 million U.S. policyholders shared telematics data with their insurer, a 28% compound annual growth rate since 2018. Carriers that connected telematics data to actual claims outcomes rather than just pricing models reported up to eight points of combined operating ratio improvement purely from the use of telematics data in claims.

Where Innovation Signals Appear

Claims activity can reveal:

- new protection needs that current products do not address

- claim journeys that create avoidable friction

- service gaps around repair, replacement, or settlement

- opportunities for specialized endorsements

- areas where digital claims support could improve the experience

- risk behaviors that may support usage-based or behavior-based products

For example, recurring EV repair complexity may support a more specialized auto product. Repeated delays in repair coordination may point to the need for stronger repair network partnerships or better digital claims updates.

How Insurers Can Respond

Product and innovation teams can use claims intelligence to:

- validate new product ideas with actual loss experience

- design endorsements around real customer needs

- improve claims communication and service workflows

- modernize products around EVs, telematics, embedded insurance, or usage-based models

- connect claims insights with customer retention and renewal strategy

Result

Claims-informed innovation helps insurers move beyond competitor-driven product development.

It gives them a clearer way to modernize products based on real policyholder behavior, actual loss outcomes, and service friction that directly affects customer trust.

Related Read: 5 Types Usage-Based Auto Insurance

Which Claims Signals Actually Require Product Action?

This section is important because one of the biggest challenges for carriers is not a lack of claims data. It is knowing which signals deserve action and which are simply noise.

Not every increase in claim activity requires a pricing change, product redesign, or underwriting adjustment. The most effective insurers focus on signals that indicate a structural change in risk, profitability, or customer behavior.

High-Priority Signals

These are signals that should typically trigger product, pricing, or underwriting review.

- Significant Severity Increases: When claim severity rises consistently within a specific segment, geography, or coverage type, it may indicate that pricing, deductibles, or underwriting assumptions are no longer aligned with actual loss costs.

- Recurring Coverage Disputes: A growing volume of disputes tied to the same policy provision often signals a product design issue rather than an isolated claims problem.

- Emerging Geographic Concentration: Rising claims activity in a specific region may indicate changing weather patterns, theft trends, litigation exposure, or other evolving risks that require product attention.

- Shifts in Litigation Activity: Changes in attorney involvement, bodily injury severity, or settlement patterns can quickly alter the economics of a product.

Medium-Priority Signals

These signals deserve monitoring but may not immediately require action.

- Temporary Frequency Fluctuations: Short-term spikes caused by seasonality, weather events, or unusual market conditions should be validated before product changes are made.

- Localized Vendor Performance Issues: Problems tied to a specific repair network, contractor, or service provider may require operational intervention before product intervention.

- One-Time Regulatory or Market Events: Certain events may temporarily influence claims outcomes without creating long-term product implications.

Low-Priority Signals

Some claims trends create visibility but rarely justify immediate product action on their own.

Examples include:

- isolated large losses

- individual fraud cases

- short-term claim anomalies

- single-event severity spikes

These events should be monitored but not automatically drive product decisions.

The Goal Is Prioritization

The objective is not to react to every claims trend. It is to identify the signals most likely to affect pricing adequacy, underwriting performance, coverage effectiveness, or portfolio sustainability.

Insurers that establish clear decision triggers can respond more consistently and avoid both overreacting to noise and underreacting to meaningful change.

Conclusion

Claims data is no longer just a record of past losses. It is becoming a product strategy asset for insurers that want to understand how risk is changing in real time.

The real advantage is not having claims data, every carrier has it. The advantage comes from detecting meaningful signals faster and turning them into product, pricing, and underwriting decisions before issues affect profitability or portfolio performance.

As an insurance strategic consultant, Practo Insura helps carriers, MGAs, and reinsurers connect claims intelligence with product strategy, underwriting discipline, and modernization initiatives, helping them build more adaptive products for changing risk conditions.

What Is Subscription Auto Insurance and How to Build It for P&C Insurer in USA

15 Apr, 2026

Auto insurance was designed for a market built on long-term vehicle ownership, predictable driving habits, and fixed policy terms.

But mobility is changing. Consumers now expect simpler billing, faster servicing, and models that align with how they access and use vehicles. As subscription-based experiences expand across industries, insurance is also beginning to shift from a rigid annual product to a more adaptable, service-led model.

That is where subscription auto insurance is gaining relevance. It gives insurers a way to align coverage with modern mobility expectations while offering customers a more flexible and convenient experience.

Understanding Subscription Auto Insurance

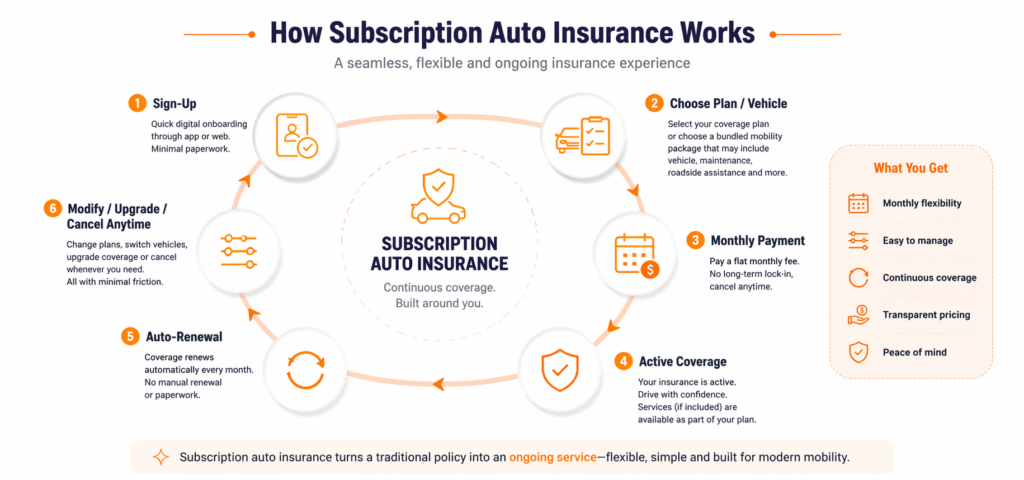

Subscription auto insurance is more than a shorter policy term. It is a different way of offering coverage.

Instead of putting customers into a fixed 6- or 12-month contract, this model usually works on a monthly recurring basis. Customers pay a flat monthly amount, coverage renews automatically, and changes like cancellation, upgrades, or vehicle swaps are meant to be much easier to handle.

What makes this model different is the way it is structured. Traditional auto insurance is built around a one-time policy purchase that is reviewed later at renewal. Subscription insurance is structured as a continuously active coverage model rather than a fixed-term contract.

It can be offered in two main ways:

- as a standalone monthly insurance product

- as part of a larger mobility package

That larger package may include:

- vehicle access

- maintenance

- roadside assistance

- insurance coverage under one monthly payment

This changes the role of insurance. Instead of being a separate product customers buy on its own, it becomes part of a broader mobility experience.

This also sets it apart from PAYG and PHYD models. PAYG is based on how much a person drives. PHYD is based on how a person drives. Subscription auto insurance is different because it is built around flexibility, simplicity, and convenience, not mileage tracking or behavioral scoring.

So, subscription auto insurance is not just a pricing change. It is a product and distribution model that makes coverage easier to package, manage, and deliver in a more service-driven way.

How Subscription Auto Insurance Works

Subscription auto insurance is designed to make coverage easier to start, manage, and continue.

In most cases, the journey begins digitally. Customers sign up online, choose a vehicle or coverage plan, and pay a flat monthly fee. Once activated, coverage renews automatically each month unless the customer decides to change or cancel it.

A typical customer journey looks like this:

- sign up through an app or website

- choose a vehicle, coverage tier, or bundled plan

- pay a monthly subscription fee

- start coverage immediately or on the selected date

- renew automatically each month

- upgrade, switch, or cancel with minimal friction

This makes the experience feel simpler than a traditional auto policy. Instead of managing a long-term insurance contract, the customer interacts with coverage as an ongoing monthly service.

How to Design a Subscription Pricing Model That Works

Pricing subscription auto insurance is not just about setting a monthly fee. The real challenge is designing a model that feels simple and predictable for customers, while still being financially sustainable for the insurer.

Unlike traditional policies, you are not pricing a fixed-term contract. You are pricing an ongoing relationship where customers can change plans, vehicles, and coverage more frequently. That makes pricing more sensitive to churn, duration, and usage patterns over time.

Core Pricing Models Used in Subscription Insurance

| Pricing Approach | How it Works | Best for | Main Advantage | Main Risk |

|---|---|---|---|---|

| Flat monthly pricing | One recurring fee for a standard coverage package | Simple direct-to-consumer offerings | Easy to understand and market | Can underprice risk if segmentation is weak |

| Tiered subscription plans | Multiple monthly plans based on coverage/service level | Insurers wanting flexibility without too much complexity | Supports upsell and clearer customer choice | Requires careful product design across tiers |

| Bundled pricing | Insurance included with vehicle/services in one fee | OEM, car subscription, mobility partnerships | Strong convenience and embedded distribution | Margin visibility and partner cost allocation can get difficult |

What Insurers Must Build Beneath the Monthly Price

Even if the monthly price looks simple to the customer, the pricing logic underneath needs to be carefully structured.

- Base monthly premium logic: Define the recurring price based on coverage level, vehicle category, and target segment. It should be built for a subscription model, not created by simply splitting an annual premium into 12 parts.

- Risk segmentation: Adjust pricing internally using factors like driver profile, geography, and vehicle type. This keeps pricing disciplined without making the customer experience feel complex.

- Bundle cost allocation: Separate the insurance portion from vehicle access or other bundled services. This is important for understanding true margins and avoiding hidden profitability issues.

- Mid-cycle pricing rules Set clear logic for vehicle swaps, plan upgrades, downgrades, or coverage changes during the subscription period. These changes should be handled smoothly without unnecessary friction.

- Proration logic: Calculate fair charges when customers make changes mid-month. This helps maintain billing accuracy while reducing revenue leakage.

Designing Pricing for Flexibility (Where Most Models Fail)

Subscription models break down when pricing cannot adapt to real-world behavior.

Your pricing design must support:

- frequent customer changes without manual intervention

- real-time or near real-time plan adjustments

- consistent billing despite mid-cycle modifications

- smooth transitions between plans or vehicles

If these are not built into pricing logic, operational friction quickly erodes the customer experience.

How to Evaluate Pricing Performance

Subscription auto insurance cannot be evaluated using traditional annual metrics alone. Performance needs to be tracked continuously, with a focus on customer behavior over time.

- Customer Lifetime Value (LTV): Measures the total value a customer generates over their full subscription period. This should factor in premium collected, claims cost, servicing cost, and retention duration. A strong model ensures LTV consistently exceeds acquisition and servicing costs.

- Monthly Churn Rate: Tracks the percentage of customers who cancel each month. Even small increases in churn can significantly reduce profitability, especially if acquisition costs are high.

- Average Subscription Duration: Indicates how long customers typically stay active. Longer durations improve profitability by spreading acquisition and onboarding costs over time. It also signals whether the product is delivering sustained value.

- Loss Ratio by Customer Cohort: Instead of looking only at overall loss ratios, insurers should track performance by customer groups (e.g., new vs retained customers, plan tiers, acquisition channels). This helps identify where risk or pricing issues are concentrated.

- Revenue Stability (Monthly Premium Consistency): Measures how predictable monthly income is across the portfolio. High volatility may indicate pricing gaps, churn issues, or overexposure to short-term customers.

- Plan Mix and Upgrade/Downgrade Trends: Tracks how customers move between pricing tiers. This helps insurers understand whether higher-value plans are being adopted and where revenue leakage may occur.

Operational Model Requirements for Subscription Insurance

Subscription auto insurance may feel simple to the customer, but it creates a more demanding operating model for the insurer.

Traditional auto insurance follows a fixed sequence: quote, bind, issue, then renew at the end of the policy term. Subscription models work differently. They run on a continuous lifecycle, where coverage is renewed monthly and customers may change plans, vehicles, or service levels far more often.

That means insurers cannot rely on operations designed for static policy administration. They need processes built for ongoing change.

Core Operational Capabilities

To run this model effectively, insurers need a few capabilities in place.

- Recurring billing and invoicing: The system must support monthly collections, payment retries, and proration when customers make changes mid-cycle.

- Rolling policy lifecycle management: Coverage needs to be managed as an active, ongoing service rather than a policy that only changes at renewal.

- Fast activation and deactivation: Customers expect coverage to start, stop, or switch quickly, without manual delays or back-office bottlenecks.

- Mid-cycle change handling: Operations must support vehicle swaps, plan upgrades, downgrades, and coverage edits at any point in the subscription period.

- Customer self-service support: Policyholders should be able to manage payments, plan changes, and account updates through digital channels without depending on manual support for every request.

Key Operational Risk Areas

The flexibility that makes subscription insurance attractive also creates operational pressure.

- Billing failures can disrupt active coverage: A missed or failed payment is not just a finance issue. If not handled properly, it can create coverage gaps, customer disputes, and compliance concerns.

- High churn increases processing volume: Frequent onboarding, offboarding, and account changes raise operational workload and can quickly strain teams that are still built around annual policy cycles.

- Bundled services increase coordination risk: When insurance is packaged with vehicle access, maintenance, or roadside services, multiple systems and partners must remain synchronized. If they do not, customer experience and margin control both suffer.

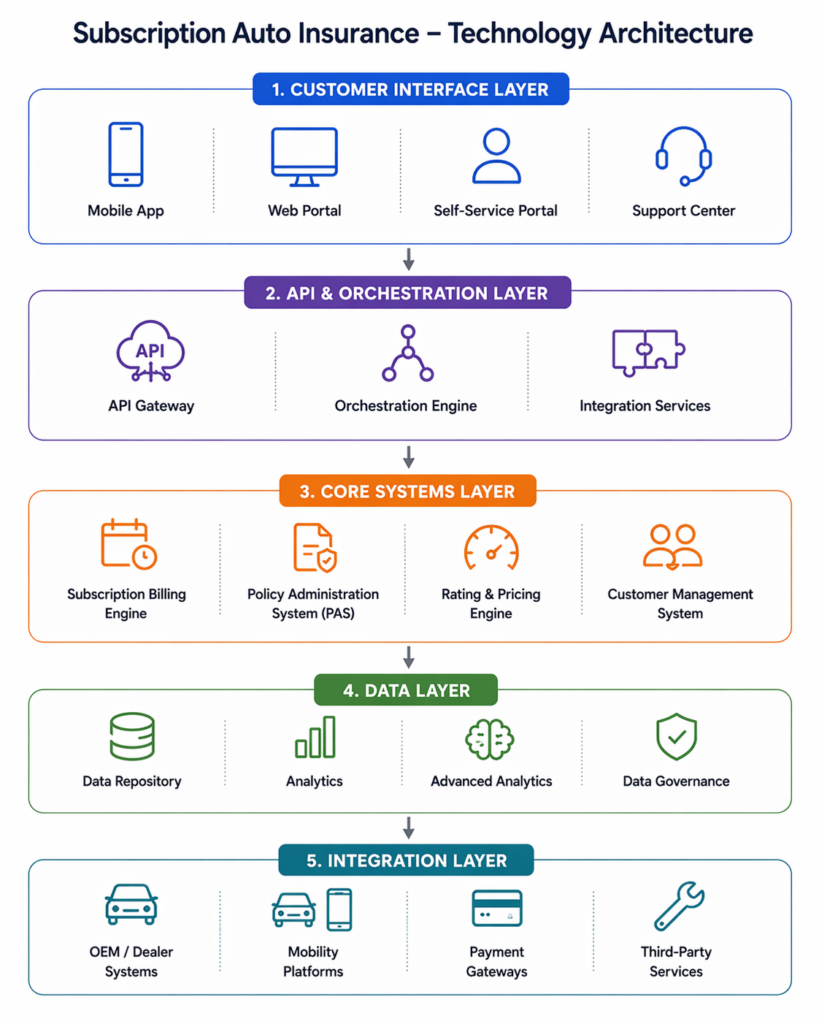

Technology Requirements for Subscription Auto Insurance

Subscription auto insurance cannot run effectively on traditional policy systems alone. The model depends on continuous updates, recurring billing, and real-time flexibility, which most legacy systems are not designed to handle.

To support this, insurers need a technology stack that enables ongoing policy orchestration, not just one-time policy issuance.

Core Technology Capabilities

To build and scale a subscription model, insurers should focus on these key components:

- Policy systems that support incremental updates:Policy administration system should allow vehicle swaps, plan changes, and coverage edits without requiring full re-issuance or manual intervention. Systems built only for fixed-term policies will struggle with this level of change.

- Billing systems designed for continuous adjustments: Monthly billing alone is not enough. The system must handle proration, failed payments, retries, and mid-cycle changes accurately and consistently at scale.

- Pricing engines that respond to event-based triggers: Rating logic should be able to update pricing when customers make changes, not just at quote or renewal. This includes plan upgrades, vehicle changes, and coverage modifications.

- Integration layers that support real-time coordination: If the product connects with OEM platforms, mobility providers, or third-party services, integrations need to be API-first and responsive. Delays between systems can create billing mismatches and poor customer experience.

- Customer platforms that enable self-service: Customers should be able to manage subscriptions, payments, and changes without manual support. This requires tightly connected front-end and core systems.

- Data systems that track behavior over time: Subscription models require visibility into churn, plan movement, and cohort performance. Data systems need to support continuous tracking, not just periodic reporting.

Integration Requirements

Subscription auto insurance rarely operates as a standalone system. In many cases, it sits inside a broader mobility ecosystem, which means insurers need strong integration across both internal and external platforms.

At a minimum, the technology stack should connect with:

- vehicle subscription platforms

- OEM and dealer systems

- mobility or ride-sharing applications

- payment gateways and billing providers

These integrations are essential for keeping pricing, billing, policy changes, and customer experience aligned across the full journey. If systems do not stay synchronized, even a well-designed product can create friction for both the insurer and the customer.

Related Read: How to Build Right Core Technology Stack for P&C Insurer in the USA

How Underwriting Changes in Subscription Auto Insurance

Underwriting in subscription auto insurance needs to work in a more dynamic environment, where coverage may change more often and customer relationships may be shorter or less stable over time. Instead of relying mainly on fixed-term assumptions, insurers need underwriting rules that can support ongoing adjustments while still protecting portfolio quality.

In practice, the biggest changes show up in a few areas:

- Eligibility needs to be tighter upfront: Clear rules are needed for which driver profiles, vehicle types, and coverage combinations are suitable. This prevents high-variability risks from entering a model designed for speed and flexibility.

- Re-rating becomes more event-driven: Pricing and underwriting should be reassessed when key changes occur, such as vehicle swaps, plan upgrades, or coverage edits. Trigger-based logic helps manage these changes without slowing down the experience.

- Shorter exposure periods need closer monitoring: Profitability can shift faster when customers stay for shorter durations. For example, a customer subscribing for one month and filing a claim early in the cycle can significantly impact margins.

- Entry and exit behavior matters more: Customers may activate coverage during high-usage periods and cancel afterward. Monitoring these patterns is critical to avoid adverse selection.

- Portfolio monitoring becomes more important: Underwriting needs to track performance by cohort, plan type, segment, vehicle category, and subscription duration to identify weak patterns early and adjust rules accordingly.

The key change is that underwriting becomes less about one-time risk assessment and more about managing risk across a product that is designed to stay flexible.

How Claims Management Needs to Change in Subscription Auto Insurance

Claims management in a subscription model needs to be built for speed, continuity, and coordination, not just settlement. Because customers can enter, exit, or modify coverage more frequently, the claims function has to operate in a way that support a model with frequent policy updates and shorter customer lifecycles.

In practical terms, insurers should focus on the following changes:

- Faster FNOL and intake workflows: Claims reporting should be instant and digital-first, with minimal steps. This reduces friction at the most critical moment and aligns with the overall subscription experience.

- Early-stage claim tracking and controls: Claims occurring soon after activation should be monitored closely, as they have a higher impact on profitability. This requires better visibility into claim timing relative to subscription start.

- Integrated service workflows: Claims systems need to connect directly with repair networks, roadside assistance, and service partners. This ensures faster resolution and avoids delays caused by disconnected processes.

- Real-time status and communication: Customers should be able to track claim progress, upload documents, and receive updates digitally. Lack of visibility can quickly impact satisfaction and retention.

- Cohort-based claims analysis: Instead of only tracking overall claims performance, insurers should analyze claims by plan type, vehicle category, acquisition channel, and subscription duration to identify patterns early.

- Flexible claims handling rules: The system should support policy changes during the claims lifecycle, such as plan upgrades or cancellations, without creating operational conflicts or manual intervention.

The key shift is that claims management needs to move from a linear, process-driven function to a more connected, real-time service layer that supports both operational efficiency and customer experience.

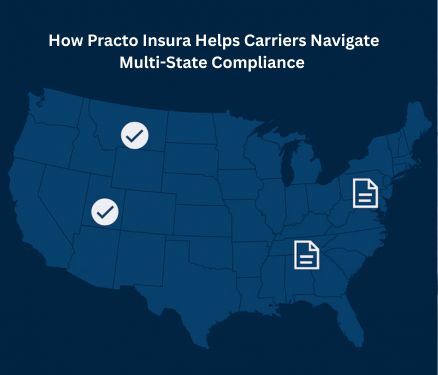

Regulatory Considerations for Subscription Auto Insurance

Subscription auto insurance introduces flexibility on the product side, but regulatory frameworks are still largely built around fixed-term policies. That creates a gap insurers need to manage carefully when designing and launching this model.

The goal is not just compliance, but ensuring that flexibility does not create regulatory risk, filing delays, or approval challenges across states.

Key Areas Insurers Need to Address

- Monthly renewal structure: Regulators may require clarity on how continuous monthly renewals are defined, whether they are treated as new policies, extensions, or a rolling contract. This impacts filings, disclosures, and compliance obligations.

- Cancellation and notice requirements: Even if the product allows easy cancellation, insurers must still comply with state-specific notice periods, non-renewal rules, and consumer protection requirements.

- Minimum coverage duration rules: Some jurisdictions may not fully support very short-term or highly flexible coverage structures. Insurers need to ensure the product aligns with minimum term expectations where applicable.

- Disclosure for bundled offerings: When insurance is packaged with vehicle access or other services, regulators may require clear separation and disclosure of:

- insurance vs non-insurance components

- pricing breakdown

- coverage terms and conditions - Filing and approval complexity: Subscription models often involve new pricing structures, billing logic, and product definitions. This can lead to:

- more detailed filings

- higher likelihood of objections

- longer approval timelines

Customer Strategy for Subscription Auto Insurance

Subscription auto insurance requires a different approach to customer strategy. Success depends not just on who you target, but on how the product fits into changing mobility needs and how clearly that value is delivered over time.

The model works best with customers whose mobility patterns are variable rather than fixed, and who are open to managing coverage as part of an ongoing service.

Target Segments to Focus On

Insurers should prioritize segments where variability in usage creates a natural fit:

- Urban and semi-urban drivers: More likely to have inconsistent driving patterns and changing vehicle needs

- Younger, digitally comfortable users: More open to managing products through apps and recurring payment models

- Subscription-oriented consumers: Already familiar with managing services through monthly payments

- Users of car subscription or leasing platforms: More likely to adopt bundled offerings where insurance is part of a broader package

- Convenience-driven, higher-income segments: Less price-sensitive and more focused on ease of management

How Insurers Should Approach Go-to-Market

Subscription auto insurance requires a different go-to-market approach compared to traditional policies.

- Embedded and partner-led distribution is a strong fit: The model aligns naturally with OEM platforms, vehicle subscription providers, and mobility ecosystems where insurance can be offered as part of a broader service

- Direct-to-consumer works when the product is simple: Clear pricing tiers and minimal configuration are critical for direct channels

- Acquisition should focus beyond price: Customers evaluate onboarding experience, billing clarity, and ease of use, not just premium levels

What Drives Customer Adoption in This Model

Adoption depends on how clearly the product fits into real usage and expectations:

- Clarity in what is included vs excluded: Customers need a clear understanding of what the monthly price covers, especially in bundled offerings

- Confidence in making changes without penalty: The ability to switch plans or vehicles without unexpected costs builds trust

- Consistency across the lifecycle: The experience from onboarding to claims should feel aligned, not fragmented

- Perceived control over the product: Customers should feel they can adjust coverage as their needs change without added complexity

Why Retention Matters More Than Acquisition

In this model, long-term value is driven more by how long customers stay than how many are acquired.

Insurers should actively manage:

- early churn, especially in the first few months

- engagement through ongoing interaction points

- clear pathways for plan upgrades or transitions

- service quality across claims and support

A customer who stays longer contributes significantly more value than one who frequently enters and exits.

When Subscription Auto Insurance Makes Sense for P&C Insurer

Subscription auto insurance is not the right fit for every insurer or every market. Before building it, insurers should assess whether the model aligns with their customer base, product design, operating model, and technology capabilities.

Decision Framework for Insurers

| Decision Area | What to Assess | Strong Fit Indicators | Warning Signs |

|---|---|---|---|

| Market fit | Whether customer demand supports a flexible monthly model | Urban or hybrid-driving markets, digital-first users, demand for convenience and lower commitment | Customers still prefer fixed annual policies and traditional billing |

| Product fit | Whether the product can be simplified into a recurring subscription structure | Standardized coverage tiers, simple monthly packaging, bundling potential | Highly customized products, complex rating structures, niche underwriting needs |

| Operational readiness | Whether internal teams can support frequent changes and continuous servicing | Ability to handle monthly billing, mid-cycle changes, fast activation, and self-service support | Heavy manual processing, slow servicing workflows, limited billing flexibility |

| Technology readiness | Whether core systems can support a subscription-based model | Modular PAS, recurring billing, real-time pricing, API integrations | Legacy systems built around fixed terms, batch processing, and limited integration |

| Regulatory fit | Whether the product can work within state-specific compliance requirements | Clear filing path, manageable disclosure needs, flexibility within target states | Unclear treatment of rolling renewals, strict cancellation rules, complex filing risk |

This model makes the most sense when there is alignment across all five areas. If one or two areas are weak, insurers may still explore the concept, but the launch path will likely be slower and more complex.

Strategic Takeaway

Subscription auto insurance is not just a product innovation. It is a business model decision. The stronger the fit across market demand, product structure, operations, technology, and compliance, the more realistic the opportunity becomes.

Conclusion

Subscription auto insurance is not just a different way to structure pricing. It requires insurers to rethink how products are designed, priced, operated, and supported across the full lifecycle.

For insurers exploring this model, the challenge is not whether the concept works. The real challenge is whether the organization is ready to support the coordination it requires across pricing, operations, technology, underwriting, and compliance.

Insurers need a structured approach to assess where the model fits, what capabilities need to change, and how to build it in a way that can scale without creating operational friction.

Insurance strategic consultants such as Practo Insura help insurers define the right model, align internal capabilities, and build the foundation needed to support subscription auto insurance effectively.

In the end, subscription auto insurance will not be defined by how innovative it looks on the surface. It will be defined by how well it is designed and executed behind the scenes

What Is Pay How You Drive Auto Insurance? How U.S. P&C Insurers Can Implement It.

03 Apr, 2026

Auto insurance pricing is already moving beyond fixed assumptions. Over the last few years, models like Pay As You Go (PAYG) have shifted pricing closer to real usage by asking a simple question: how much does someone drive?

Pay How You Drive (PHYD) takes that one step further. Instead of focusing only on mileage, it looks at something more telling, how that mileage is actually driven.

At its core, PHYD is a behavior-based insurance model where premiums are influenced by real driving patterns captured through telematics. Rather than relying primarily on traditional rating factors like age, ZIP code, or historical proxies, insurers begin to incorporate observed driving behavior into pricing decisions.

According to research, insurers using behavioral pricing models can improve risk segmentation accuracy by up to 30%.

This changes the role of data in underwriting. Instead of estimating risk upfront and leaving it largely static, PHYD allows insurers to continuously refine their view of risk based on how a policyholder actually behaves on the road.

Understanding the Pay How You Drive Insurance

PHYD is a behavior-based pricing model.

Premiums are adjusted based on continuous assessment of driving quality, not just miles accumulated. The insurer collects granular telematics data, processes it through a behavioral scoring engine, and applies a score-derived modifier to the base premium.

The key distinction from PAYG is that PHYD is not an exposure correction. It is a risk quality correction.

How Pay How You Drive Insurance Works

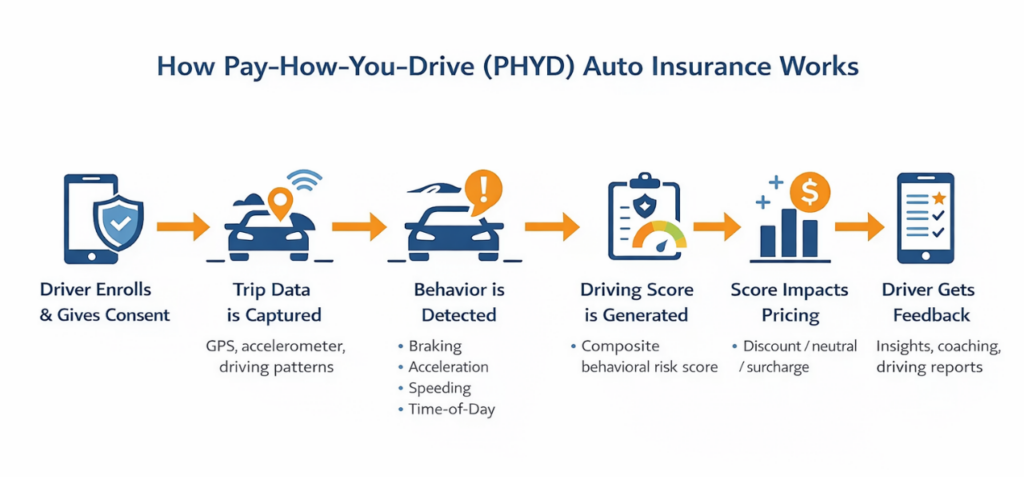

While the underlying technology can be complex, the customer and insurer journey typically follows a clear sequence:

- Enrollment and Consent: The policyholder opts into the program, agreeing to share telematics data through a mobile app, device, or connected vehicle system.

- Trip Data Collection: Each trip is recorded using sensors such as GPS and accelerometers, capturing movement, speed, and driving patterns.

- Behavioral Event Detection: The system identifies specific driving events, for example, hard braking, rapid acceleration, speeding, or late-night driving.

- Score Generation: These events are processed into a composite driving score, reflecting the overall risk profile of the driver.

- Pricing Adjustment: The score is translated into a pricing outcome, typically a discount, neutral adjustment, or surcharge, applied at renewal or, in some cases, during the policy term.

- Feedback Loop: Drivers receive insights or summaries of their driving behavior, creating a continuous feedback cycle between behavior and pricing.

This structured flow is what differentiates PHYD from simpler usage-based models. It is not just tracking activity, it is interpreting behavior and linking it directly to risk.

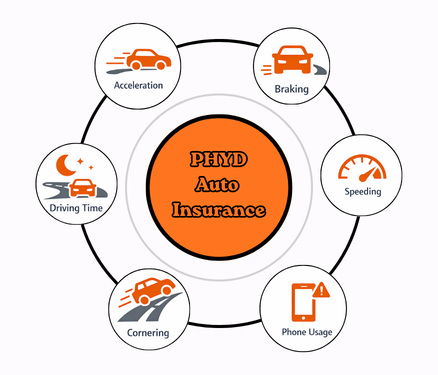

Behavioral Signals That Drive the Score in PHYD

The variables most predictive of loss frequency and severity are:

- Hard braking events: the strongest single predictor of loss frequency

- Rapid acceleration: correlated with aggressive driving patterns

- Speeding above posted limits: primary severity driver

- Time-of-day driving concentration: elevated risk in nighttime hours

- Phone distraction proxies: screen-state + motion fusion signals

Pricing Architecture & Behavioral Scoring for Pay How You Drive Auto Insurance

If PHYD changes how risk is observed, pricing architecture is where that insight turns into measurable financial impact.

At a structural level, PHYD does not replace traditional ratings. Instead, it layers behavioral intelligence on top of it, allowing insurers to refine pricing based on how risk is expressed over time, not just how it is assumed at policy inception.

This creates a dual-layer model where traditional underwriting establishes the baseline, and behavioral scoring adjusts that baseline dynamically.

Types of Pricing Structure in PHYD

Most PHYD programs follow a consistent structure:

- Base Premium: Calculated using traditional rating variables such as vehicle, coverage, territory, and driver history.

- Behavioral Modifier: A percentage-based adjustment applied on top of the base premium, reflecting observed driving quality over a defined scoring window.

In practice, this means two drivers with identical starting profiles may diverge over time based on how they actually drive. Pricing becomes less about assumed risk and more about continuously observed behavior.

Discount vs. Surcharge Design

The pricing design in PHYD is not just about adjustment, it’s about how risk is introduced into the product over time.

Most insurers begin with a discount-only model, where safer driving leads to lower premiums, but risky behavior does not immediately result in penalties. This reduces customer resistance and simplifies regulatory approval.

As data maturity improves, insurers shift toward bidirectional pricing, introducing both discounts and surcharges. This allows pricing to better reflect actual risk and helps maintain loss ratio discipline, especially for consistently high-risk drivers.

In-Term vs. Renewal Adjustment

Another core design choice is when behavioral data impacts pricing.

In renewal-based models, pricing is updated at the start of each policy term using past driving data. This approach is stable and easier to operate but slower to reflect behavior changes.

In in-term models, pricing adjusts during the policy period based on ongoing data. This improves accuracy but requires real-time billing capability and clear communication to avoid customer confusion.

Behavioral Variables & Pricing Impact on Insurance Premiums

Behavioral scoring is built on telematics-derived variables that demonstrate measurable relationships with loss outcomes. Each variable must be carefully selected, validated, and weighted based on its predictive strength.

| Variable | Measurement Method | Pricing Impact | Primary Data Source |

|---|---|---|---|

| Hard braking | Accelerometer - G-force threshold breach | High - strong loss frequency predictor | Mobile SDK / OBD-II |

| Rapid acceleration | Accelerometer + GPS speed change | Moderate-High | Mobile SDK / OBD-II |

| Speeding | GPS speed vs. posted limits (map-integrated) | High - linked to severity and frequency | GPS + map layer |

| Time-of-day driving | Trip timestamp segmentation (e.g., night driving) | Moderate -elevated risk periods | Mobile app / OEM feed |

| Phone distraction | Device sensor + screen interaction patterns | High - proxy for distracted driving | Mobile SDK |

| Cornering / handling | Gyroscope + accelerometer data | Moderate | Mobile SDK / OBD-II |

| Behavioral consistency | Pattern stability across trips | Low–Moderate | Scoring engine |

Not all variables carry equal weight. Insurers typically prioritize those with stable and statistically credible relationships to loss frequency, while continuously evaluating emerging signals such as distraction.

Score Translation to Pricing Bands

Once behavioral data is captured, it must be translated into a usable pricing signal.

Most PHYD programs aggregate individual variables into a normalized composite score, often on a 0-100 scale. This score is then mapped into pricing bands such as 'Excellent', 'Good', 'Fair' & 'High-Risk'.