For decades, U.S. auto insurance has been structured around fixed six- or twelve-month policies that assume vehicles are exposed to risk continuously. This model works well for drivers who use their vehicles daily, but it becomes less accurate when actual driving patterns are irregular or intermittent.

Today, mobility behavior is changing. Remote work, hybrid schedules, and urban transportation alternatives mean many drivers use their vehicles only occasionally. As digital services in other industries become more flexible and on-demand, some consumers are beginning to expect insurance products that align coverage and pricing more closely with when vehicles are actually being used.

Usage-based auto insurance is rapidly gaining traction. According to Fortune Business Insights, the global UBI market is expected to grow from $43 billion in 2023 to more than $149 billion by 2030, reflecting increasing demand for flexible, exposure-based insurance products.

Understanding Pay-As-You-Need (PAYN) in Auto Insurance

Pay-As-You-Need (PAYN) auto insurance is an on-demand coverage model where coverage is active only during specific driving periods. Instead of maintaining continuous coverage for months at a time, drivers activate insurance when they plan to use the vehicle.

Coverage can be structured around defined activation windows such as a trip, a set number of hours, or a full day. Once the selected coverage period ends, protection also ends unless the policyholder activates it again. This approach ties insurance exposure directly to vehicle usage rather than assuming constant driving risk.

How Pay-As-You-Need Insurance Works

Operationally, PAYN auto insurance works through a real-time coverage activation model. A typical PAYN journey looks like this:

- Driver opens the insurance app: The policyholder accesses the PAYN policy through the insurer’s mobile platform.

- Driver activates coverage before the trip: Coverage is turned on before the vehicle is used.

- Coverage becomes active immediately: The insured period starts in real time based on product rules.

- Trip is monitored during the active period: Telematics or trip-detection tools may verify vehicle usage during coverage.

- Coverage ends when the trip ends: Protection turns off once the trip ends or the selected time expires.

- Premium is calculated based on active exposure: The insurer prices coverage based on duration and applicable risk factors.

Depending on product design, coverage may be structured per trip, per hour, or per day. This is essentially a form of micro-duration insurance, where protection is tied to short, specific periods of vehicle use rather than continuous annual exposure.

Related Read: 6 Types of On Demand Auto Insurance and Who They Fit Best

Designing a Pay-As-You-Need Auto Insurance Product

Designing a PAYN auto insurance product requires insurers to rethink how coverage activation and exposure are structured within the policy lifecycle. While the underlying protections remain similar to traditional auto insurance, the operational design must support short-duration coverage periods.

Key product design considerations to include:

- Coverage activation rules

- Minimum coverage windows

- Idle vehicle exposure management

- Activation frequency limits

These decisions shape how flexible the product becomes while still maintaining actuarial and operational stability.

Strategic Opportunities in Pay-As-You-Need Coverage

PAYN auto insurance gives insurers an opportunity to design more flexible, usage-aligned products that reflect how vehicles are actually used. As driving patterns become less predictable, PAYN can help insurers align premiums with real exposure while also strengthening digital engagement with policyholders.

Customer Segments That Pay-As-You-Need Auto Insurance Can Serve

PAYN products can be particularly valuable for segments where vehicle usage is irregular or situational:

- Occasional drivers: Individuals who use their vehicles only a few times per week or for specific errands.

- Urban vehicle owners: Drivers living in cities where public transport, rideshare, or walking reduce regular car usage.

- Gig economy drivers: Drivers who need insurance coverage that aligns with when they are actively working.

- Low-mileage drivers: Policyholders whose annual mileage is significantly below average and who may feel traditional premiums do not reflect their actual exposure.

By targeting these segments, insurers can introduce new product formats, attract digitally engaged customers, and experiment with flexible insurance models that better reflect evolving mobility behavior.

Types of Pricing Models in Pay-As-You-Need Insurance

Pricing in Pay-As-You-Need (PAYN) insurance is designed for active exposure, not continuous annual use. Instead of charging for assumed year-round driving, insurers price coverage only for the time or trip window when the policy is turned on. This gives product teams more flexibility to create pricing models that match how the vehicle is actually being used.

Insurers can structure PAYN pricing in several ways, including:

- Trip- or time-based pricing: Premium is charged based on each insured trip or time window, such as per hour or per day.

- Base activation fee plus usage charge: The insurer applies a minimum activation fee and adds a variable charge based on actual usage.

- Subscription plus on-demand usage pricing: The driver pays a recurring access fee, with additional premium charged only when coverage is activated.

- Risk-adjusted dynamic pricing: Premium changes in real time based on exposure factors such as driver profile, vehicle, location, and trip conditions.

- Minimum-duration pricing: The insurer sets a minimum billable coverage period even when the actual trip is shorter.

In all these models, the goal is the same: to make premium more closely reflect the specific risk present during the insured period rather than relying entirely on annual exposure assumptions.

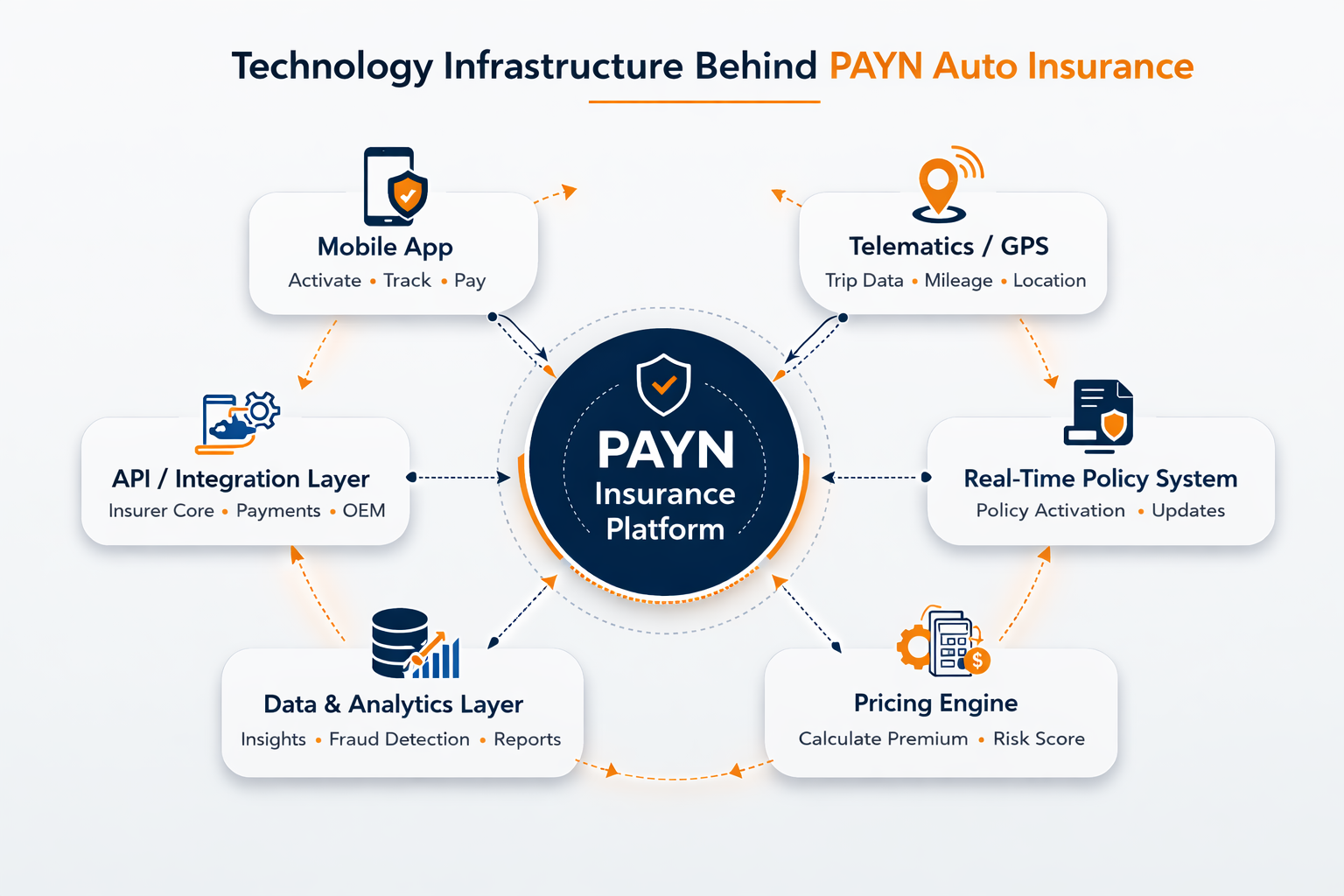

Technology Infrastructure Supporting Pay-As-You-Need Insurance

Delivering Pay-As-You-Need auto insurance requires a digital-first technology ecosystem capable of supporting real-time policy activation, exposure tracking, and short-duration coverage management.

Below are technology components required to support PAYN insurance operations:

- Mobile insurance platforms: Mobile applications allow drivers to activate coverage, monitor policy status, and manage PAYN policies in real time.

- Telematics and trip-detection technology: GPS and telematics tools help verify when a trip starts and ends, supporting accurate exposure tracking.

- Real-time policy administration systems: Core insurance systems must be able to activate coverage instantly, update policy status, and issue micro-duration policies.

- Dynamic pricing engines: Rating systems calculate premiums based on exposure variables such as trip duration, location, and driver risk characteristics.

- Data and analytics platforms: These platforms analyze driving patterns, exposure data, and usage trends to support underwriting and product optimization.

- API-based integration layers: APIs connect mobile apps, telematics systems, pricing engines, and policy administration platforms to ensure real-time communication across systems.

Underwriting Considerations for Pay-As-You-Need Policies

PAYN changes the underwriting approach because exposure is intermittent and short duration. Instead of relying on annual driving assumptions, underwriters must evaluate risk across individual trips, activation patterns, and usage contexts.

Key underwriting considerations include:

- Driving frequency: Insurers need to understand how often the vehicle is actually used, even if coverage is not active continuously.

- Trip timing: Risk can vary significantly depending on whether trips occur during daytime, late-night hours, weekends, or peak traffic periods.

- Geographic exposure: Underwriters may need to evaluate whether trips occur in low-density suburban areas, congested urban corridors, or higher-risk zones.

- Behavioral risk indicators: Telematics and usage data can help identify patterns such as harsh braking, speeding, route type, or inconsistent activation behavior.

- Coverage activation behavior: PAYN introduces the risk that drivers may try to activate coverage only for selected trips while avoiding activation in situations they perceive as lower value or higher risk.

A major concern is adverse selection, where drivers may activate coverage only for certain trips. To manage this, insurers may use controls such as minimum activation windows, lead times, subscription fees, and telematics-based trip verification.

Claims Management in Pay-As-You-Need Insurance

Claims handling in PAYN insurance requires insurers to verify that coverage was active at the time of the accident. Because PAYN policies operate on short activation windows, claims teams must confirm the exact timing of coverage before processing the claim.

Key elements typically verified during a PAYN claim include:

- Coverage activation timestamp: Confirming when the policy was activated through the mobile platform.

- Trip start and end times: Determining whether the accident occurred during the insured driving window.

- Accident timestamp: Matching the reported accident time with the active coverage period.

- Accident location: Verifying where the incident occurred using telematics or GPS data.

Telematics and trip data can play an important role in PAYN claims processing. These systems can help insurers reconstruct trip timelines, verify driving activity, and detect inconsistencies between reported events and recorded vehicle movement.

Telematics data can significantly improve claims validation. Deloitte estimates that connected vehicle data can reduce fraud and claim disputes by 20-40%

Regulatory Considerations for Pay-As-You-Need in the United States

PAYN auto insurance must still comply with state-level insurance regulation in the U.S. Even though coverage is activated for short periods, insurers still need to meet the same core regulatory standards that apply to other auto insurance products.

Key regulatory considerations include:

- SERFF filings: PAYN products must be filed through SERFF with rates, rules, and forms for state approval.

- Actuarial support: Pricing must be justified and not considered unfairly discriminatory.

- Minimum liability compliance: Short-duration coverage must still meet state financial responsibility requirements.

- Clear coverage triggers: Policy forms must define when coverage starts, ends, and how activation works.

- Consumer disclosures: Insurers must clearly explain activation rules, coverage windows, and billing logic.

- DOI review: State DOIs may closely assess whether PAYN creates liability coverage gaps.

- Telematics disclosure: If GPS or telematics is used, carriers may need clear consent and data-use language.

- State-by-state variation: PAYN filings may need to differ by jurisdiction based on local auto insurance rules.

5 Operational Challenges P&C insurers Face in Implementing PAYN

Implementing PAYN auto insurance requires insurers to support real-time coverage activation, short-duration policies, and dynamic pricing. This often introduces operational complexity, especially for carriers relying on legacy insurance systems.

Key challenges insurers may face include:

- Legacy policy administration systems: Many existing core systems are built for annual policies and may struggle to handle real-time activation and micro-duration coverage.

- Real-time policy processing: PAYN requires systems that can instantly activate, update, and deactivate coverage without delays.

- System integration complexity: Mobile apps, telematics tools, pricing engines, and policy systems must communicate seamlessly in real time.

- Customer education and experience: Drivers must clearly understand how to activate coverage and when they are insured.

- Fraud prevention risks: Insurers must prevent issues such as post-accident activation or manipulation of trip data through verification controls.

Conclusion

Pay-As-You-Need (PAYN) auto insurance reflects a broader shift toward aligning insurance coverage with actual driving exposure rather than assumed annual usage. As mobility patterns become more dynamic and digital engagement increases, models like PAYN allow insurers to offer coverage that activates only when needed while maintaining strong risk alignment.

For U.S. P&C insurers, implementing PAYN requires more than a new pricing construct. It calls for coordinated decisions across product architecture, underwriting, policy administration, distribution readiness, and regulatory execution. As an insurance strategic consultant, Practo Insura helps carriers assess PAYN market fit, define go-to-market strategy, and translate the concept into an operationally viable auto product.

We specialize in developing innovative Property & Casualty (P&C) insurance software solutions, leveraging over 8 years of InsurTech expertise to simplify insurance operations and enhance efficiency.

Share Article via

Subscribe to our insights newsletter

Related Blog Posts

Insurance Underwriting Automation: Implementation Guide...

12 Jun, 2026

12 Jun, 2026

Most P&C underwriters did not join the industry to chase...

Read More

Why Claims Data Matters in...

03 Jun, 2026

Claims data has traditionally been treated as a record of...

Read More

What Is Subscription Auto Insurance...

15 Apr, 2026

Auto insurance was designed for a market built on long-term...

Read More