Choosing the right Policy Administration System (PAS) is one of the most important technology decisions for insurers, MGAs, and agencies. A modern PAS goes beyond processing policies, it drives faster product launches, improves compliance, supports digital customer service, and reduces manual work.

With so many solutions available, the best choice depends on your business model, size, and regulatory needs. In this guide, we review ten leading PAS platforms for the P&C industry, highlighting their features, pros and cons, and best use cases so you can decide which system fits your goals.

Best P&C Insurance PAS System in USA

1. Duck Creek

Duck Creek has established itself as a leading PAS for Property & Casualty insurers who demand both agility and enterprise-grade robustness. Its cloud-native architecture, regular release cadence, and strong support for compliance make it popular among carriers modernizing away from legacy systems.

With the pressure from regulatory demands, faster product launches, and customer expectations for digital self-service, Duck Creek aims to be a platform that balances strategic flexibility with operational stability.

Key Features

- Evergreen SaaS model with automatic bi-weekly updates, reducing the need for large re-implementations.

- Low-code / no-code product configuration tools so insurers can adjust business rules, pricing, workflows without heavy IT involvement.

- Open architecture and extensive API support, enabling integration with portals, external services, data sources.

- Scalable support across multiple lines of business (personal, commercial, specialty), plus strong regulatory compliance features (reporting, audit).

- Self-service portals for policyholders & agents, multi-channel communication (email, web, mobile).

Pros & Cons

| Pros | Cons |

|---|---|

| High speed to market: fast product rollout due to configurable templates and frequent updates. | Implementation complexity: carriers with highly customized legacy processes may need substantial rework. |

| Robust compliance and scalability, support multi-state / multi-jurisdiction regulatory reporting out of the box. | Cost: premium pricing, both for licensing and ongoing feature upgrades; not always optimal for very small agencies. |

Best Used For

- Operationally, it shines when the insurer wants to shift “business rule changes” and product configuration out of IT silos into business teams, thus reducing dependencies and shortening product launch cycles. Also ideal for those needing strong agent/insured self-service and behavior-driven workflows.

- Strategically, Duck Creek is best when a large or mid-sized P&C carrier needs to modernize its core policy administration, reduce technical debt, and elevate its agility in launching new product lines or entering new jurisdictions. Carriers that are burdened by frequent regulatory changes or need strong audit/compliance capabilities will gain high value.

G2 Review: 4.6/5

2. Vertafore (MGA Systems)

Vertafore’s MGA Systems is built for MGAs, program administrators, and wholesalers. It focuses on giving them the speed and flexibility they need for quoting, binding, issuing policies, handling commissions, and creating detailed reports.

When underwriting, program launches, or broker workflows get complicated, MGA Systems helps bring everything into one place and automates many of the manual tasks.

Key Features

- Workflow and raters for quoting, binding, issuing policies.

- Automated renewals & endorsements.

- Accounting modules: payables, receivables, commissions.

- Document generation and storage.

- Open APIs, data/code access, custom reporting including carrier feeds and bordereaux.

- Multi-currency and international support (for MGAs operating cross-border).

Pros & Cons

| Pros | Cons |

|---|---|

| Very well suited to MGA use-cases: speed, flexibility, commission handling, reporting requirements. | For large carriers with deeply complex underwriting / risk models, may lack depth in actuarial or bureau functionalities. |

| Strong reporting, ability to generate custom outputs (bordereaux, carrier data feeds) helps meet compliance and partner needs. | Custom setup and connecting to many external systems may take time; cost of scaling may rise as volume increases. |

Best Used For

- Strategically, MGAs and program administrators who operate in multiple states or lines, need fast product rollouts, and who are responding to broker/agent demands for digital portals and transparency.

- Operationally, when quoting & binding, commission processing, renewals & endorsements have become bottlenecks; when agents or brokers require feeding data into partner carriers and reporting or data aggregation is required; or when MGAs want to standardize workflows across offices or regions.

G2 Review: 4.3/5

3. Practo Insura

Practo Insura is a relatively newer entrant in the U.S. P&C PAS landscape, positioning itself for mid-size carriers and MGAs who need flexibility, speed, and lower friction in product launches. It emphasizes rapid rating, data migration, built-in business intelligence, predictive analytics for underwriting and modern architecture.

In a market where many insurers are still held back by aging, fragmented systems or manual workflows, Practo Insura appeals where agility matters without sacrificing compliance or reliability.

Key Features

- Rapid Rater algorithm enabling new rate implementation in ~7 days.

- Self-service portal for policyholders and insureds for payment, document access, policy change requests.

- Built-in business intelligence & workflow analytics to identify bottlenecks.

- Real-time MVR (motor vehicle record) detection for fraud/risk management.

- Custom e-sign tool and high service levels (uptime, security).

Pros & Cons

| Pros | Cons |

|---|---|

| Very fast product/rate deployments; less dependency on long IT cycles. | As a newer system, may have fewer “proven large scale” enterprise deployments. |

| Enhanced risk-management features (MVR, fraud tools) and modern UX. |

Best Used For

- Strategically, mid-size P&C carriers or MGAs seeking to expand or enter new states, wanting agility in product/rate changes and emphasis on risk management as well as compliance. Also, useful where speed and modern digital touchpoints are part of differentiation strategy.

- Operationally, for organizations that want automation in underwriting/rating, want actionable BI and analytics, self-service tools for agents/insureds, and wish to reduce manual intervention and legacy migration cost.

4. Origami Risk

Origami Risk delivers a unified SaaS platform aimed at insurers, MGAs, and program administrators who want end-to-end coverage: digital underwriting, rating, billing, claims, analytics, and portals.

Its strength is configurability and deep integration of bureau content with user-friendly dashboards and role-based access. Especially important in lines where underwriting/granting authority or variability is high, Origami Risk lets clients adapt quickly.

Key Features

- Support for out-of-sequence endorsements, quotes, binds, renewals.

- Agency relationship management, flexible commission calculations/payouts.

- Configurable workbench dashboards per role (underwriter, CSR, etc.).

- Built in analytics tools; import latest bureau content for rating.

- Integrated billing, payments, invoicing with policy lifecycle management.

- Headless portals (agent / insured) and API integration for external systems.

Pros & Cons

| Pros | Cons |

|---|---|

| Highly configurable: rating and underwriting logic can be updated without heavy custom coding. | For very large enterprises or highly customized legacy systems, migration may be nontrivial. |

| Full suite with analytics and bureau content support, reducing need for many third-party add-ons. | Scaling to the very highest transaction volumes or geographies might expose performance or support constraints (depending on implementation). |

Best Used For

- Strategically, Origami Risk works well when a carrier or MGA needs a single platform that supports underwriting, rating, claims, billing, and analytics together, especially in specialty or bureau-dependent lines. Also, when commission flexibility and role-based dashboards are important for regulatory audit, performance oversight, and underwriting authority control.

- Operationally, it’s ideal when agents or insureds need portals; when renewals and endorsements across multiple lines are frequent; when you want digital touchpoints and billing integration; and when time to market for new rates/policies needs to be fast.

G2 Review: 4.5/5

5. Brite Core

Brite Core is a cloud-native policy administration system targeting P&C carriers looking for modern architecture, automation, and strong agent/insured engagement features. Carriers moving from legacy systems, seeking to improve user experience, reduce manual interventions, and provide transparent portals often consider Brite Core.

Key Features

- Straight through processing for new business, renewals, cancellations via business-rules engines.

- Real-time endorsement handling including backdated, future-dated, and out-of-sequence changes.

- Agent/insured portals for access to policy documents, payments, status.

- Notifications/triggers and engagement metrics (e.g. document opens, clicks) to track policyholder engagement.

- Audit trail: detailed logs, alerts, reminders.

Pros & Cons

| Pros | Cons |

|---|---|

| Very strong UX and modern front-end for agents and policyholders; reduces calls and manual support. | May require careful change management; not all legacy data or specialized workflows will map cleanly. |

| Good automation and endorsement flexibility reduce operational drag. | For large multi-jurisdiction/regulation heavy carriers, may need extra configuration or customization. |

Best Used For

- Strategically, for carriers that want to improve policyholder experience, reduce overhead from manual tasks (endorsements & portals), and differentiate on customer touchpoints. Also, appropriate when insurer is growing and needs scalable cloud architecture.

- Operationally, Brite Core suits companies focusing on digital portals, need frequent policy adjustments, endorsements, and renewals, and wanting to automate communications & engagement metrics.

G2 Review: 4.3/5

Related Read: How to Audit Your Current Policy Administration System for Insurance Teams

6. Riskonnect

Riskonnect brings together policy administration capabilities with an explicit focus on risk analytics, certificate management, and loss control tools. For carriers and MGAs that view risk mitigation as central, not peripheral, its offering is compelling.

In a P&C landscape where regulatory exposure, under-insurance, and risk leakage are under sharper scrutiny, Riskonnect aims to help insurers avoid surprises, improve precision, and streamline certificates and risk-management workflows.

Key Features

- Anomaly detection and premium leakage identification.

- Certificate issuance, tracking, expiration management.

- Loss control tools integrated with underwriting or workflow steps.

- Workflow automation and product configuration tools.

- Broker/agent/insured self-service portals; mobile/web enabled.

- Reporting & analytics dashboard for risk, exposures, certificate status.

Pros & Cons

| Pros | Cons |

|---|---|

| Strong risk visibility helps reduce exposure, detect anomalies early, and manage certificates (often a pain point). | More specialized: those who don’t need heavy certificate or loss control tools may not fully leverage it. |

| Workflow automation and rich analytics help reduce manual effort and improve decision quality. | Might have higher setup/integration effort, especially with existing underwriting or billing systems. |

Best Used For

- Strategically, Riskonnect is best for carriers or MGAs that put risk control at the center of their business. It’s especially useful for policies that require a lot of certificates (like commercial or umbrella lines), or for companies facing strict regulatory oversight. It also helps when issues like premium leakage or compliance risks need more visibility.

- Operationally, it’s helpful when issuing and tracking certificates takes too much manual effort, when premium or risk anomalies need quick detection, and when agents or brokers need easier portals and clearer access to information.

G2 Review: 4.2/5

7. Applied Epic

Applied Epic is more agency/MGA-oriented, offering a comprehensive AMS that covers P&C and Benefits lines. It combines quoting, policy management, accounting, commissions, renewals, and more in a single platform.

Key Features

- Full lifecycle: prospecting, quoting, binding, policy management, renewals, accounting.

- Integrated Benefits workflows (rates, TPAs, eligibility).

- Dashboards and analytics for performance & renewal forecasting.

- Omnichannel customer service / agent portal / mobile app connectivity.

- Flexible APIs and integration capacity with insurer systems.

Pros & Cons

| Pros | Cons |

|---|---|

| Very strong for agencies managing multiple lines and offices; reduces need for multiple disconnected tools. | Might lack the deep underwriting / risk tools required by large commercial carrier operations. |

| Excellent connectivity with insurers, strong ecosystem, mature platform. | Custom configuration and integration can be time consuming; licensing / cost scales with usage. |

Best Used For

- Strategically, Applied Epic works well for agencies or MGAs that want to grow across different lines of business, improve client service and retention, and get clearer insight into renewals and commissions. It’s a good fit for agencies moving from multiple separate tools to one unified system.

- Operationally, it’s ideal when quoting, servicing, accounting, and renewals are scattered across systems. By bringing everything together, it helps agents work faster, and client portals and mobile access make customers happier.

G2 Review: 4.4/5

8. EZLynx

EZLynx is designed for independent agencies that want an affordable, all-in-one system to manage quoting, binding, renewals, claims, payments, and servicing. It brings these features together in one cloud platform, cutting down on duplicate data entry and making daily work smoother.

Key Features

- End-to-end lifecycle: quotes, binds, claims, service, renewals.

- Automation Center: triggers for renewals, quote proposals, claims updates.

- Integrated suite: quote system, retention tools, management dashboards.

- Single unified data view for policy, claims, documents.

- Carrier downloads/data feeds to keep policy data current.

Pros & Cons

| Pros | Cons |

|---|---|

| Very good value for agencies; reduces the number of separate tools needed. | Limited support for highly customized commercial lines underwriting or large schedule complexities. |

| Great automation, retention tools, and streamlined data flow improve productivity. | May lack the depth of bureau compliance, regulatory reporting, or very advanced underwriting analytics. |

Best Used For

- Strategically, independent agencies or small-to-mid MGAs that want to improve client responsiveness, reduce administrative burden, and use digital tools (portals, automation) for service differentiation.

- Operationally, when workflows for renewal, quoting, policy servicing are slowing down due to multiple tools / manual data entry; when agencies want to give customers and agents online access; or when foot traffic/client service calls are high and digital self-service helps reduce load.

G2 Review: 4.3/5

9. Insurity

Insurity positions itself as a PAS solution for insurers with large, complex policy books and frequent regulatory or bureau content updates. The system is built to meet the needs of commercial, specialty, and personal lines insurers where policy complexity, high schedule loads (many vehicles or locations per policy), and endorsements are routine

Key Features

- Fully managed bureau change updates, so clients do not have to separately track or implement bureau requirements.

- Support for large schedules (e.g. thousands of locations or vehicles per single policy) with out-of-sequence (OOS) endorsements and high transaction volume.

- Modern API-first platform and connectivity for digital distribution channels.

- Intelligent underwriting rules and automation to handle complex risk logic.

- Focus on compliance and regulatory reporting.

Pros & Cons

| Pros | Cons |

|---|---|

| Very strong for high-complexity policies; capable of handling large schedules and complex endorsements smoothly. | Might be overkill (cost/time) for smaller carriers or those with simpler lines of business. |

| Bureau management and regulation support reduce risk and compliance burden. | User interface and modern UX may lag newer entrants in polish; potential learning curve. |

Best Used For

- Strategically, Insurity is a strong option for insurers that write complex commercial or specialty lines and face frequent regulatory changes. It’s also a good fit for companies that need to manage large policy portfolios with many endorsements or schedules.

- Operationally, it works well for insurers that process high volumes of transactions and large policies. It reliably handles out-of-sequence endorsements, connects with third-party data sources, and helps maintain strict compliance requirements.

G2 Review: 3.7/5

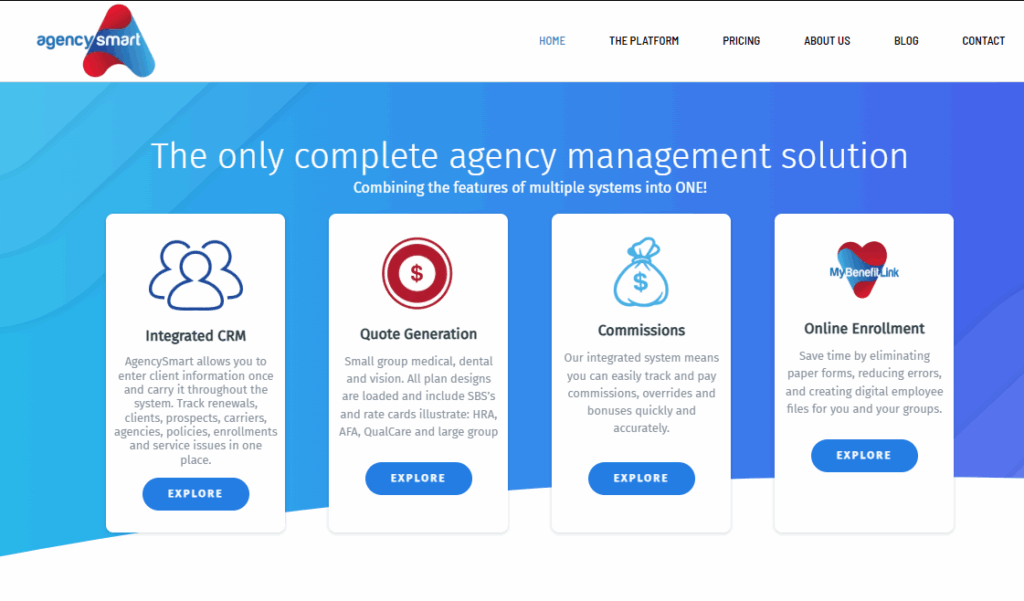

10. Agency Smart

Agency Smart is designed for insurance agencies and brokers who want one cloud platform to handle quoting, enrollments, commissions, and servicing. It helps cut down on duplicate data entry, reduce mistakes, and give a clearer view of each client’s journey. This makes it especially useful for small and mid-size agencies that may currently rely on spreadsheets or a mix of disconnected tools.

Key Features

- Integrated CRM for client tracking, prospects, renewals, policy/enrollment/service.

- Quoting tools for small group medical/dental/vision with rate cards and plan designs.

- Commissions management: overrides, bonuses, payments.

- Online enrollment/self-management for employees.

- Mobile / tablet / laptop support.

Pros & Cons

| Pros | Cons |

|---|---|

| Streamlines agency operations; reduces redundant data entry and improves accuracy. | Not built for large commercial underwriting complexities; limited in scope for large-scale endorsements or bureau requirements. |

| Good fit for benefits, small group quoting, and online enrollment workflows. | May grow less cost-efficient / feature constrained for agencies expanding into heavy regulatory or commercial lines. |

Best Used For

- Strategically, agencies (and small-to-mid MGAs) that want to level up their operations, improve client experience through faster quoting, make commissions and enrollment more transparent, and reduce manual overhead.

- Operationally, when multiple disconnected tools or spreadsheets slow down quoting, renewals, or service; when errors / rework is common, when agents/employees need mobile or remote access; or when self-service is expected by clients.

G2 Review: 4.8/5

Comparison Matrix: Top 10 PAS Providers in P&C Insurance

| Vendor | Key Differentiators | Pros | Cons | Best Fit |

|---|---|---|---|---|

| Duck Creek | Evergreen SaaS, bi-weekly updates, low/no-code config, strong API ecosystem | Fast time to market, enterprise scale, strong compliance | High cost, complex implementation | Large & mid-tier carriers modernizing core PAS and needing compliance strength |

| Insurity | Large/complex schedule handling, managed bureau updates | Excellent for bureau/regulatory, handles thousands of risks per policy | May be too heavy for smaller carriers, UI not as modern | Carriers in commercial/specialty lines with complex endorsements and compliance needs |

| Practo Insura | Rapid Rater (7-day rollout), BI & analytics, risk/fraud tools | Speed to market, modern UX, strong self-service | Newer entrant, fewer legacy integrations | Mid-size carriers & MGAs expanding state-to-state needing agility and digital portals |

| Origami Risk | Unified PAS + billing + claims, ISO/NCCI bureau integration | Configurable underwriting, strong analytics & portals | Migration complexity for very large carriers | Carriers & MGAs needing integrated claims, billing, bureau compliance |

| Brite Core | Cloud-native, strong agent/insured portals, advanced endorsements | Great UX, automation reduces workload | May need extra config for complex multi-jurisdiction carriers | Regional/mid-size P&C insurers seeking digital portals & automated workflows |

| Riskonnect | Risk visibility tools (anomaly detection, loss control, certificates) | Strong risk insights, streamlined certificate management | More specialized for risk-heavy business, higher setup effort | Commercial carriers & MGAs focusing on risk analytics, certificates, compliance |

| Applied Epic | Most widely used AMS; P&C + Benefits | Strong insurer connectivity, unified AMS | Not deep on underwriting/risk tools, complex setup | Growth-focused agencies and MGAs managing multiple lines and offices |

| EZLynx | Affordable all-in-one for agencies, automation center | Cost-effective, improves agency workflows | Not suited for complex underwriting or bureau-heavy carriers | Independent agencies needing simple, affordable PAS with automation |

| Vertafore | Purpose-built for MGAs/program admins, custom reporting & bordereaux | Strong MGA workflows, flexible APIs | Not suited for full carrier PAS | MGAs/wholesalers needing rapid product launch & complex reporting |

| Agency Smart | Cloud AMS, small group quoting, integrated CRM | Simplifies agency ops, reduces errors | Limited commercial line depth, feature set smaller | Small to mid-size agencies focusing on benefits, quoting, commissions |

Choosing the Right PAS for Your P&C Business

Modern PAS solutions give insurers and agencies the tools to compete in a fast-changing market. Whether you need enterprise-scale flexibility, bureau compliance, risk management tools, or an affordable all-in-one system for agencies, there is a platform built for your needs.

The right PAS helps reduce costs, improve client satisfaction, and prepare your organization for future growth. By matching your strategic priorities and day-to-day operations with the right system, you can turn policy administration from a back-office task into a true competitive advantage.

We specialize in developing innovative Property & Casualty (P&C) insurance software solutions, leveraging over 8 years of InsurTech expertise to simplify insurance operations and enhance efficiency.

Share Article via

Subscribe to our insights newsletter

Related Blog Posts

Insurance Underwriting Automation: Implementation Guide...

12 Jun, 2026

12 Jun, 2026

Most P&C underwriters did not join the industry to chase...

Read More

Why Claims Data Matters in...

03 Jun, 2026

Claims data has traditionally been treated as a record of...

Read More

What Is Subscription Auto Insurance...

15 Apr, 2026

Auto insurance was designed for a market built on long-term...

Read More