U.S. P&C insurers are spending more on technology than ever before, and yet, many carriers still struggle with legacy systems that slow product launches, create compliance risks, and frustrate policyholders. That’s because modern insurance performance doesn’t start with customer experience; it starts with core technology.

Your core tech stack is the foundation of your operating model. It powers how policies are issued, claims are settled, billing is processed, and data is analyzed. Without a modern stack, even the best front-end portals or CX tools can’t deliver speed, accuracy, or compliance at scale.

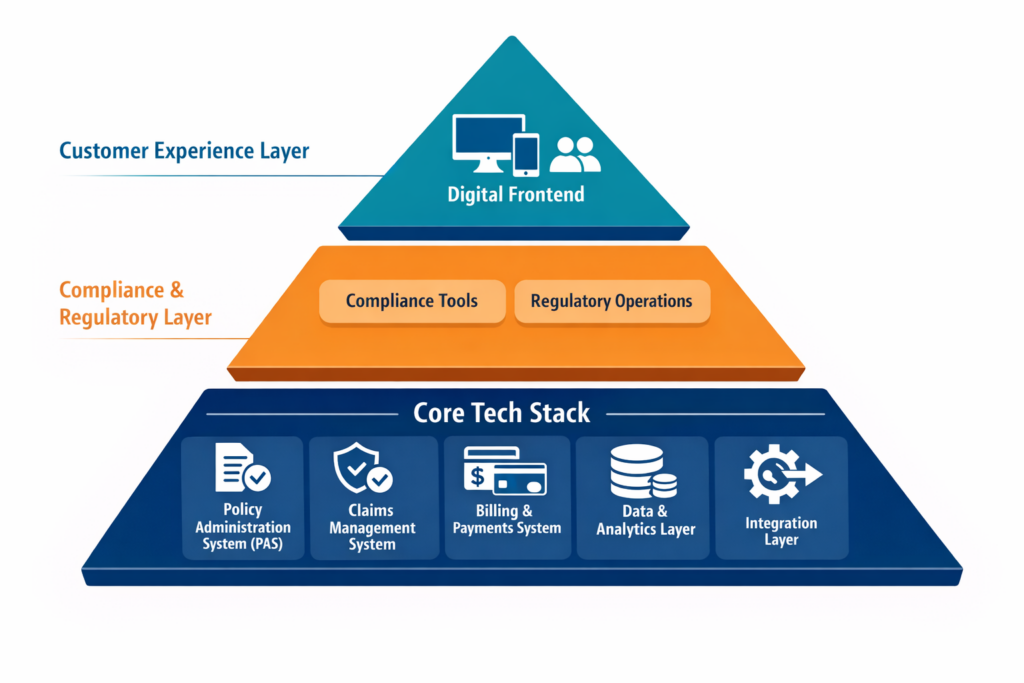

What Is Considered as Core Tech?

In the context of a modern U.S. P&C insurer, your core technology stack isn’t about flashy AI or digital front ends, it’s about the mission-critical systems that underpin your insurance operations. These are the technologies that directly support quoting, binding, servicing, billing, claims handling, and regulatory compliance

Core tech sits below your customer experience (CX) and compliance layers. It’s what keeps the business running before a chatbot responds, an agent logs in, and a filing is submitted to a DOI.

Here are the five components that make up the core stack:

- Policy Administration System (PAS): The operational core of insurance. It manages product definitions, ratings, quoting, issuance, endorsements, renewals, and cancellations. Think of it as your “product engine”.

- Claims Management System: Handles first notice of loss (FNOL), adjudication, approvals, and payouts. It’s critical for customer trust and operational cost control.

- Billing & Payments System: Manages invoicing, collections, commissions, refunds, and digital payment integrations. A key driver of both cash flow and customer satisfaction.

- Data & Analytics Layer: Serves as the backbone for reporting, pricing, actuarial work, operational dashboards, and regulatory analytics. Without this, insights stay siloed.

- Integration Layer: Serves as a connective tissue. It enables these systems to work together through APIs, event triggers, and shared workflows. It also links your core stack with CRM, portals, regulatory systems, and AI tools.

Together, these systems form the foundation of scalability. When chosen and configured properly, they allow for faster product launches, better compliance, and more automated servicing.

How to Select Right Core Technologies?

1. How to Select the Right Policy Administration System (PAS)

A modern Policy Administration System is the core of your insurance product engine. Everything else, claims, billing, portals, and compliance, ultimately relies on the data and structure the PAS provides.

What Functionalities Should a PAS Cover?

A robust PAS should support these key functionalities:

- Product Configuration & Rating: Define insurance products, coverage types, rating rules, and eligibility logic with minimal code.

- Quoting & Underwriting Workflows: Automate quote generation, risk assessment, and referral logic for speed and consistency.

- Policy Issuance & Document Generation: Seamless generation of bindable policies, notices, endorsements, and forms.

- Mid-Term Endorsements & Renewals: Support for lifecycle servicing without disrupting compliance tracking.

- Multi-State Compliance Support: Ability to adapt to jurisdictional differences in forms, rates, and rules.

- Version Control & Audit Trails: Full traceability across policy lifecycle changes to meet DOI and internal governance needs.

Why PAS Is Foundational?

Your PAS doesn’t just handle policies, it defines how your insurance products behave across every channel and process. It’s the single source of truth for coverage logic, rate application, compliance enforcement, and downstream data. A weak PAS leads to quoting errors, compliance gaps, and slower market entry. A strong PAS sets the rhythm for your entire operation.

Key Evaluation Criteria When Selecting a PAS

When evaluating a PAS, insurers should assess:

- Architecture Requirements: Cloud-native, API-first, modular design that supports scalability, containerization, and version upgrades with low downtime.

- Functional Coverage: Out-of-the-box support for personal/commercial lines, ISO integration, rate/test environments, and full policy lifecycle servicing.

- Data Capabilities: Structured data model, event-driven updates, and support for data lineage, essential for analytics, filings, and claims triggers.

- Operational Fit: Role-based access, workflow configurability, task queues, and bulk operations that align with underwriting and servicing models.

- Compliance Enablement: Jurisdiction-aware rule logic, filing documentation exports, and audit-ready logs help streamline SERFF filings and DOI inquiries.

2. How to Select a Claims Management System?

While the PAS governs the structure of insurance products, the claims system plays a critical role in fulfilling the insurer’s contractual obligations. It’s the part of your operation that directly affects the customer’s experience, how quickly, fairly, and smoothly a claim is handled.

What Functionalities Should a Claims Management System Cover?

A modern claims platform should support:

- First Notice of Loss (FNOL) Intake: Multi-channel FNOL capture (web, phone, email, mobile app) with structured triage logic.

- Automated Adjudication Rules: Configurable rules engine for routing, approvals, and fraud detection without constant IT involvement.

- Adjuster Workflows & Case Management: Assign tasks, manage caseloads, track SLAs, and escalate exceptions with full visibility.

- Vendor Integration & Payment Processing: Support for third-party services like repair shops, loss assessors, or medical networks, with seamless disbursements.

- Communications & Document Management: Templates, correspondence logs, e-signatures, and claim package automation for clear stakeholder communication.

- Reserving & Recovery Management: Built-in support for financial reserving, subrogation, and salvage to ensure accurate loss ratios and recoverables.

Why Claims Management System Matters in Core?

Claims isn’t just about payouts, it’s about delivering on the policy promise. Poor claims systems create operational delays, leakage, and litigation risks. A well-designed claims platform builds trust, improves outcomes, and reduces cost per claim, all while feeding valuable data back into underwriting and actuarial models.

Key Evaluation Criteria When Selecting a Claims System

When selecting a claims management system, insurers should evaluate:

- Architecture Requirements: API-first with workflow engines, event triggers, and flexible deployment (cloud, hybrid, or on-prem) for future-proof scalability.

- Functional Coverage: End-to-end support for FNOL to closure across multiple LOBs, including property, auto, liability, and specialty.

- Efficiency & Automation: Low-code workflows, straight-through processing (STP) without manual intervention, automatic adjudication based on coverage and thresholds, and proactive fraud flagging.

- Data Management: Real-time reporting dashboards, loss ratio visibility, integration with PAS for coverage validation, and audit logs for compliance.

3. How to Select a Billing & Payments System?

Billing isn’t just about collecting premiums, it’s a major touchpoint in the policyholder journey. Your system needs to support flexible plans, multiple payment channels, agent commissions, and clear financial reconciliation.

What Should a Billing System Cover?

Key capabilities of a modern insurance billing system include:

- Invoicing & Statement Generation: Automates invoice schedules, reminders, and dunning letters based on billing plans and premium frequency.

- Payment Processing: Accepts multiple methods, ACH (Automated Clearing House), credit/debit cards, digital wallets, and supports integrations with processors and gateways.

- Commission Handling: Tracks agent/broker commissions, overrides, and adjustments with full audit visibility.

- Installment & Recurring Plans: Enables flexible billing frequencies (monthly, quarterly, annual) and supports mid-term changes.

- Refunds, Cancellations & NSFs: Automates processing of refunds, cancellations for non-payment, and handling of bounced or declined payments.

- Reconciliation & Financial Reporting: Connects to general ledger systems and provides real-time dashboards for receivables, cash application, and audits.

Why Billing System Is Core?

Billing and payments touch every insured, every policy, every month. The system must balance financial accuracy, operational efficiency, and user experience. A strong billing engine also ensures compliance with premium collection laws, state cancellation rules, and finance charges, while giving insureds the payment flexibility they expect.

Checklist to Select Right Billing Technology

When evaluating billing systems, insurers should assess:

- Architecture Requirements: Look for modular, cloud-native systems with support for secure payment integrations, PCI compliance, and containerized services.

- Functional Fit: Ensure the system can handle both direct and agency billing, billing plan variations, commission hierarchies, and real-time payment updates.

- Payment Capabilities: Support for autopay, third-party payments, refunds, and split payments, with tokenized card storage and fraud monitoring.

- Finance & Compliance Readiness: Built-in reconciliation tools, state-specific cancellation logic, notice templates, and financial audit trails to meet statutory and GAAP requirements.

4. How to Select the Data & Analytics Layer?

A modern insurer can’t operate effectively without a strong data foundation. The data layer powers everything from pricing and claims trends to regulatory reporting and AI models. Without it, teams are stuck with siloed reports, outdated spreadsheets, and blind spots across operations.

What Should a Data Layer Cover

The data & analytics layer should enable:

- Enterprise Data Consolidation: Brings together structured and unstructured data from PAS, claims, billing, CRM, and third-party systems into a central repository or lake.

- Operational Dashboards & Reporting: Provides role-specific dashboards for underwriting, claims, finance, and compliance, updated in real time.

- Regulatory & Compliance Analytics: Enables timely filings, DOI responses, and internal audits with traceable, structured data.

- Predictive Modeling & Actuarial Insights: Supports pricing, reserving, and risk modeling with access to clean, reliable historical and real-time data.

- Embedded AI/ML Capabilities: Allows integration of machine learning models for loss prediction, churn risk, and segmentation directly into workflows.

- Data Lineage & Governance: Tracks how data flows and transforms, ensuring transparency, auditability, and trust.

Why Data & Analytics Layer is Important

The data layer is not just for analysts, it underpins every major decision across product, claims, compliance, and operations. With growing regulatory scrutiny and the rise of AI-driven processes, insurers need real-time, connected, and governed data pipelines.

Checklist to Select Right Data Platforms

When assessing your data & analytics solution, consider:

- Architecture Requirements: Scalable cloud-based lakes or warehouses with support for APIs, batch/stream processing, and secure access layers for users and models.

- Functional Capabilities: Out-of-the-box dashboard templates, embedded reporting tools, real-time data ingestion, and support for custom model deployment.

- Advanced Requirements: Must support data lineage tracking, consent-based data usage, audit logs, anonymization capabilities, and integration with external benchmarks or rating bureaus.

5. How to Select the Integration Layer?

Your systems are only as powerful as how well they work together. A strong integration layer ensures seamless data flow across policy, billing, claims, portals, analytics, and external partners. It’s what enables insurers to operate as a connected ecosystem, not isolated silos.

Why the Integration Layer Matters

As insurers adopt more SaaS tools, AI services, and third-party platforms, manual handoffs and brittle point-to-point integrations become liabilities. A modern integration layer improves agility, simplifies upgrades, and accelerates digital transformation by connecting systems through reusable, scalable pipelines.

It’s especially critical for carriers adopting layered modernization, where not everything is replaced at once, and legacy + modern systems must co-exist.

Integration Layer Requirements

Your integration architecture should support:

- Support for APIs: Ability to expose and consume secure RESTful APIs for all core services (quote, bind, claim, billing, documents, etc.), with full documentation and authentication layers (OAuth2, JWT, etc.).

- Event-Driven Architecture: Publish/subscribe capability to emit real-time events to trigger downstream workflows and notifications.

- Workflow Orchestration: Ability to coordinate multi-step business processes across systems, including retries, human-in-the-loop actions, and approval flows.

- Monitoring & Observability: Centralized logging, health checks, and real-time monitoring dashboards to detect integration failures or data lags before they affect CX or compliance.

10 Common Mistakes to Avoid When Building Your Core Tech Stack

Even well-resourced insurers make strategic missteps when modernizing core systems. Avoiding these pitfalls can save years of rework, tech debt, and compliance exposure.

- Choosing Tech Without Defining Target Operating Model: Don’t start with software, start with your ideal process. Otherwise, you’ll force-fit tech into legacy workflows.

- Underestimating the Role of Data in PAS Design: Many PAS projects fail because data models aren’t structured for rating, reporting, or regulatory filings across states.

- Ignoring Claims Workflow Configurability: If business users can’t adjust claims rules or SLAs without IT, turnaround times will suffer long after go-live.

- Fragmented Billing Across Direct & Agency Channels: Running separate billing systems for agents and policyholders leads to inconsistent records, lost commissions, and reconciliation headaches.

- Treating Analytics as a Post-Implementation Add-On: Waiting to address data architecture after core rollout creates silos. Embed analytics from day one.

- Overengineering Integrations: Hard-coded point-to-point integrations are brittle and expensive to maintain. Use an API-first, event-driven approach.

- Neglecting Compliance Triggers in Core Systems: Missing state-specific cancellation rules, DOI audit logs, or rate versioning logic creates regulatory risk.

- Choosing Systems That Don’t Support Layered Modernization: If your core stack can’t coexist with legacy systems during transition, the migration will stall or fail.

- Relying Only on Vendors, Not Consultants: Tech vendors sell software. Strategic insurance partners helps you design the right stack for your growth, filings, and CX goals.

- Overlooking User Experience for Internal Teams: If underwriters, adjusters, or billing teams hate the UI, adoption will lag, no matter how “modern” the backend is.

Conclusion

Whether you’re a regional carrier expanding into new states or an MGA bringing niche products to market, your success depends on choosing the right systems for policy admin, claims, billing, analytics, and integration. These aren’t isolated decisions. They shape your ability to launch compliant products, operate efficiently, and deliver exceptional service.

But building the right core stack isn’t just about selecting tools with the most features. It’s about aligning technology with your operating model, compliance strategy, and long-term business goals. It’s about ensuring each layer, from PAS to data pipelines, works together as a coordinated whole.

That’s where strategic consulting makes a difference. Partners like Practo Insura help carriers go beyond software selection, offering architecture guidance, regulatory insight, and implementation strategies tailored to U.S. P&C insurers. The result? Systems that not only work, but work for you.

We specialize in developing innovative Property & Casualty (P&C) insurance software solutions, leveraging over 8 years of InsurTech expertise to simplify insurance operations and enhance efficiency.

Share Article via

Subscribe to our insights newsletter

Related Blog Posts

Insurance Underwriting Automation: Implementation Guide...

12 Jun, 2026

12 Jun, 2026

Most P&C underwriters did not join the industry to chase...

Read More

Why Claims Data Matters in...

03 Jun, 2026

Claims data has traditionally been treated as a record of...

Read More

What Is Subscription Auto Insurance...

15 Apr, 2026

Auto insurance was designed for a market built on long-term...

Read More