Claims data has traditionally been treated as a record of past losses, used mainly for reserving, reporting, and post-event analysis. But in today’s U.S. P&C market, where repair severity, litigation exposure, climate volatility, and emerging risks are changing faster than traditional product cycles, claims data is becoming a strategic input for product design, pricing, and underwriting decisions.

The real challenge is no longer whether insurers have claims data, every carrier does. The challenge is how quickly they can convert claims signals into business action. As the gap between changing risk conditions and organizational response widens, claims intelligence is becoming a critical capability for improving underwriting performance, product relevance, and long-term profitability.

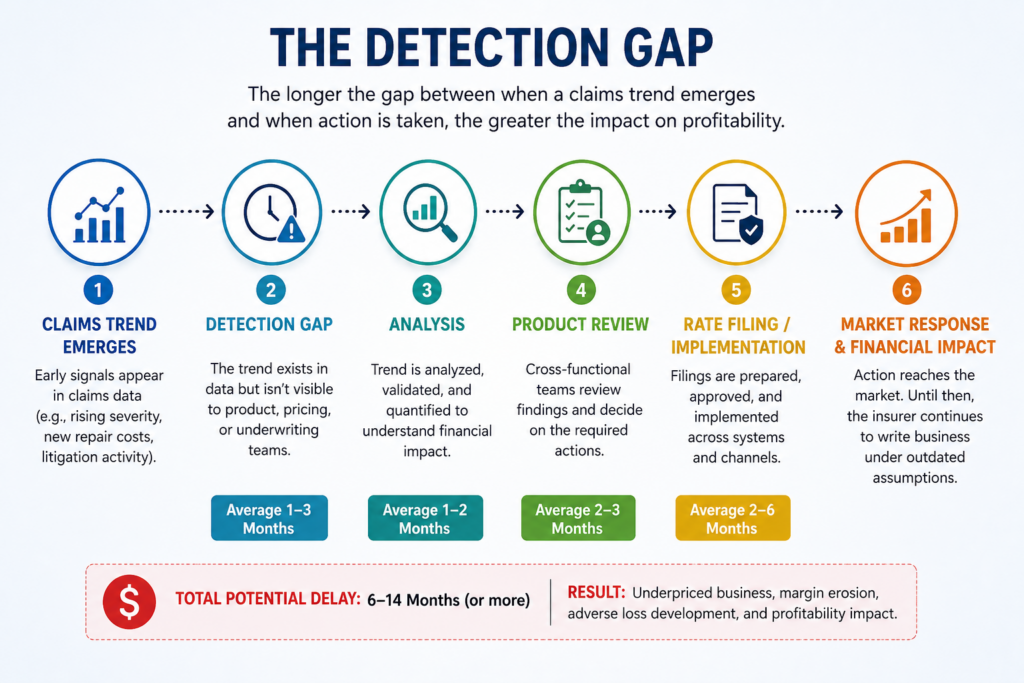

What is Detection Gap in Modern Insurance Product Design

Most carriers do not struggle because they lack claims data. They struggle because there is often a significant gap between when a claims trend emerges and when the organization takes action.

Consider a common auto insurance example. Claims teams may start seeing higher repair severity for specific vehicle segments due to increasing ADAS calibration requirements, longer repair cycles, or more expensive replacement parts. The signal exists. The data exists. The problem is that product, underwriting, and pricing teams may not see that trend until months later through formal reviews or profitability reporting.

That delay creates what can be called the Detection Gap, the period between when claims data first signals a meaningful change in risk and when the organization responds with a pricing, underwriting, or product adjustment.

Why the Detection Gap Matters

The financial impact of a claims trend is rarely immediate. Instead, it accumulates quietly across hundreds or thousands of policies before it becomes visible in portfolio-level metrics.

- A severity trend may emerge today.

- A product team may detect it three months later.

- Analysis and validation may take another two months.

- A rate filing may require several more months before implementation.

By the time corrective action reaches the market, an insurer may have spent nearly a year writing business under assumptions that no longer reflect actual risk conditions.

The challenge is not limited to auto insurance. Similar detection gaps appear across P&C lines through:

- emerging weather-related loss patterns

- litigation-driven bodily injury severity

- coverage disputes and claims escalation trends

- organized fraud activity

- geographic concentration risk

In many cases, claims activity identifies these issues long before they appear in underwriting profitability reports.

From Claims Data to Business Action

Closing the detection gap requires insurers to think differently about claims information.

Claims data alone has limited value. What matters is how quickly that data becomes actionable intelligence.

The progression looks like this:

Claims Data → Pattern Detection → Business Decision → Product Action

The faster an organization moves through this cycle, the faster it can:

- adjust pricing assumptions

- refine underwriting appetite

- redesign coverage structures

- manage emerging risks

- protect portfolio profitability

This is why leading insurers increasingly treat claims intelligence as a strategic product management capability rather than a claims reporting function.

Why Claims Data Has Become a Strategic Product Asset

Claims data was once treated mainly as an operational record: what happened, what was paid, and how claims were handled. But for modern P&C insurers, that view is too limited.

Every product decision eventually shows up in claims. Pricing decisions affect profitability. Underwriting rules affect loss frequency. Coverage wording affects disputes. Deductibles affect claim behavior. Geographic expansion affects concentration risk.

That is why claims data has become a strategic product asset. It helps insurers validate whether product assumptions still match real-world risk conditions before problems appear in high-level profitability reports.

For carriers, MGAs, and reinsurers, the value is not simply having more claims data. The value is converting claims signals into faster pricing, underwriting, coverage, and portfolio decisions.

1. Validating Pricing and Underwriting Decisions

Pricing and underwriting decisions are built on assumptions. Claims data is where those assumptions are tested against actual loss behavior.

A rate plan may assume that a certain vehicle class, territory, driver profile, or coverage type carries a predictable level of risk. But once claims begin developing, insurers can see whether that assumption still holds. This is especially important in auto insurance, where repair severity, bodily injury trends, litigation involvement, and vehicle technology can change the economics of a segment quickly.

The impact is already visible in repair data. According to industry research, the average total cost of repair has increased 96.4% since 2009, rising from approximately $2,405 to more than $4,720 in 2024. Nearly half of that increase occurred within the last five years alone. ADAS-related costs are a major contributor. Calibration fees increased from $168 in 2017 to $488 in 2024, while diagnostic-related costs per 100 claims grew from roughly $580 to more than $21,300.

At the same time, auto insurance claims have increased 14% since 2020, while claims severity has risen 36%. For product and underwriting teams, these trends demonstrate how quickly actual loss costs can diverge from historical pricing assumptions.

What Claims Data Helps Validate

Claims data can show whether:

- certain vehicle types are producing higher severity than expected

- specific territories are generating more frequent or more expensive claims

- bodily injury trends are worsening in particular states

- deductible structures still make sense for current repair costs

- underwriting rules are attracting the right risk profile

- rating variables are still aligned with actual loss outcomes

For example, if newer vehicles with advanced safety systems are consistently producing higher repair costs than expected, the issue is not just claims severity. It may indicate that the current pricing model, deductible design, or underwriting assumptions need to be refined.

What Insurers Can Do With This Insight

Product and underwriting teams can use claims intelligence to make targeted changes, such as:

- revising rating factors

- adjusting deductible options

- tightening eligibility rules

- updating underwriting guidelines

- modifying territory assumptions

- flagging specific segments for pricing review

- redesigning coverage structures where loss behavior has changed

This prevents claims insight from staying trapped inside claims operations. It turns the data into a practical input for product and underwriting decisions.

The Result

When insurers use claims data to validate pricing and underwriting assumptions, they gain a clearer view of where the product is still working and where it is drifting away from real risk.

The result is sharper segmentation, better risk selection, stronger rate adequacy, and more disciplined portfolio management.

Related Read: How Insurers Use Predictive Analytics to Improve Underwriting and Risk

2. IdentifyingCoverage Gaps and Emerging Risks

Claims activity often reveals a different kind of product problem: not whether the price is right, but whether the coverage itself still works in the real world.

A product may be priced correctly and still create friction if policy wording is unclear, endorsements are outdated, limits no longer reflect current costs, or new exposures were not considered when the product was designed. These issues usually surface during claims, when customers test the product under actual loss conditions.

What Claims Data Reveals

Claims data can show:

- which coverages generate the most disputes

- where policy language creates confusion

- which endorsements are producing unexpected loss behavior

- whether limits or deductibles still match current repair and replacement costs

- where new risks, such as EV repairs, severe weather, or litigation trends, are creating product pressure

For example, an auto insurer may find that rental reimbursement limits are no longer adequate because repair cycle times have increased. A property insurer may see repeated disputes around water damage or storm-related exclusions. An MGA may discover that a niche endorsement is being used differently than originally expected.

What Insurers Can Do With This Insight

Product teams should treat these patterns as design feedback, not just claims friction.

That means insurers can:

- review dispute trends by coverage type

- analyze escalation patterns tied to specific policy wording

- reassess limits, deductibles, and exclusions against current claim realities

- update endorsements where loss behavior has changed

- involve claims and compliance teams before product changes are finalized

The Result

Using claims data this way helps insurers close coverage gaps before they become larger profitability, litigation, or customer experience problems.

It also makes product design more grounded in real claim behavior, not just market assumptions, competitor forms, or historical coverage structures.

3. Reducing Fraud and Claims Leakage

Fraud is not always obvious at the individual claim level. One inflated repair supplement, one represented injury claim, or one unusual billing pattern may look isolated. The real signal appears when similar patterns repeat across vendors, geographies, coverages, or claim types.

That is where claims intelligence becomes valuable. It helps insurers move beyond claim-by-claim review and identify leakage patterns that point to broader product or process vulnerabilities.

A 2024 study by CLARA Analytics found that AI-driven cohort modeling identified potential fraud indicators within two weeks of claim submission. Approximately 9% of open claims were flagged as strong SIU referral candidates, with the model identifying suspicious activity at a rate comparable to experienced adjusters but significantly earlier in the claim lifecycle.

Where Leakage Often Shows Up

Common signals include:

- repeated supplement requests from specific repair vendors

- abnormal medical billing patterns

- recurring use of the same coverage provisions

- staged accident indicators

- unusual claim timing or clustering

- claim types with higher-than-expected escalation rates

For example, if a specific endorsement is repeatedly involved in questionable claims, the issue may not be limited to fraud investigation. The endorsement itself may need clearer eligibility rules, stronger documentation requirements, or tighter claim controls.

How Insurers Can Respond

Insurers can reduce leakage by:

- standardizing vendor and provider tracking

- connecting SIU findings with product and underwriting teams

- reviewing claim pathways that are repeatedly exploited

- tightening documentation requirements where abuse patterns appear

- monitoring fraud indicators by coverage, vendor, geography, and claim type

Result

This helps insurers reduce avoidable claim costs while improving product discipline.

More importantly, it turns fraud detection into a product feedback mechanism. If claims data shows where the product is being exploited, insurers can redesign the exposure instead of only investigating it after the loss occurs.

Related Read: 5 Questions Every Carrier Must Ask Before Launching a New Line of Business

4. Improving Product Profitability and Portfolio Performance

Growth can hide weakness in a P&C portfolio. A product may continue adding premium while certain geographies, coverages, or customer segments quietly produce more volatility than expected.

Claims intelligence helps insurers separate healthy growth from fragile growth.

According to AM Best, the P&C industry’s combined ratio improved from 101.6 in 2023 to 96.6 in 2024, driven in part by stronger pricing discipline, improved underwriting performance, and broader use of analytics.

Where Portfolio Pressure Often Appears

Claims data can reveal:

- geographies with concentrated or worsening loss activity

- coverages creating unexpected volatility

- segments requiring stronger reserve attention

- claim types affecting reinsurance confidence

- products where growth is outpacing risk control

- business classes producing unstable loss development

For example, a carrier may expand successfully in written premium, but claims activity may show that one region is becoming more exposed to weather losses or litigation-heavy claim behavior. That does not always mean the product should exit the market. It may mean the insurer needs tighter appetite rules, different deductibles, revised limits, or a different reinsurance view.

How Insurers Can Respond

Product, underwriting, and portfolio teams can use claims intelligence to:

- identify where growth should be accelerated, slowed, or restricted

- evaluate product performance below the portfolio-average level

- reassess limits, deductibles, and appetite by region or segment

- use claim volatility trends in reinsurance planning

- decide whether certain products need redesign before expansion continues

Result

Claims-informed portfolio management helps insurers grow with more discipline.

It gives leadership a clearer view of which parts of the portfolio are sustainable, which require correction, and which may create future volatility if left unmanaged.

5. Accelerating Product Innovation and Customer Experience Improvements

Product innovation does not always start with a new idea. Sometimes it starts with repeated claims patterns that show where customers need better protection, clearer service, or a product built for newer risk behavior.

Claims data gives insurers a practical view of how products perform after purchase, when the policyholder actually needs the coverage.

In 2024, more than 21 million U.S. policyholders shared telematics data with their insurer, a 28% compound annual growth rate since 2018. Carriers that connected telematics data to actual claims outcomes rather than just pricing models reported up to eight points of combined operating ratio improvement purely from the use of telematics data in claims.

Where Innovation Signals Appear

Claims activity can reveal:

- new protection needs that current products do not address

- claim journeys that create avoidable friction

- service gaps around repair, replacement, or settlement

- opportunities for specialized endorsements

- areas where digital claims support could improve the experience

- risk behaviors that may support usage-based or behavior-based products

For example, recurring EV repair complexity may support a more specialized auto product. Repeated delays in repair coordination may point to the need for stronger repair network partnerships or better digital claims updates.

How Insurers Can Respond

Product and innovation teams can use claims intelligence to:

- validate new product ideas with actual loss experience

- design endorsements around real customer needs

- improve claims communication and service workflows

- modernize products around EVs, telematics, embedded insurance, or usage-based models

- connect claims insights with customer retention and renewal strategy

Result

Claims-informed innovation helps insurers move beyond competitor-driven product development.

It gives them a clearer way to modernize products based on real policyholder behavior, actual loss outcomes, and service friction that directly affects customer trust.

Related Read: 5 Types Usage-Based Auto Insurance

Which Claims Signals Actually Require Product Action?

This section is important because one of the biggest challenges for carriers is not a lack of claims data. It is knowing which signals deserve action and which are simply noise.

Not every increase in claim activity requires a pricing change, product redesign, or underwriting adjustment. The most effective insurers focus on signals that indicate a structural change in risk, profitability, or customer behavior.

High-Priority Signals

These are signals that should typically trigger product, pricing, or underwriting review.

- Significant Severity Increases: When claim severity rises consistently within a specific segment, geography, or coverage type, it may indicate that pricing, deductibles, or underwriting assumptions are no longer aligned with actual loss costs.

- Recurring Coverage Disputes: A growing volume of disputes tied to the same policy provision often signals a product design issue rather than an isolated claims problem.

- Emerging Geographic Concentration: Rising claims activity in a specific region may indicate changing weather patterns, theft trends, litigation exposure, or other evolving risks that require product attention.

- Shifts in Litigation Activity: Changes in attorney involvement, bodily injury severity, or settlement patterns can quickly alter the economics of a product.

Medium-Priority Signals

These signals deserve monitoring but may not immediately require action.

- Temporary Frequency Fluctuations: Short-term spikes caused by seasonality, weather events, or unusual market conditions should be validated before product changes are made.

- Localized Vendor Performance Issues: Problems tied to a specific repair network, contractor, or service provider may require operational intervention before product intervention.

- One-Time Regulatory or Market Events: Certain events may temporarily influence claims outcomes without creating long-term product implications.

Low-Priority Signals

Some claims trends create visibility but rarely justify immediate product action on their own.

Examples include:

- isolated large losses

- individual fraud cases

- short-term claim anomalies

- single-event severity spikes

These events should be monitored but not automatically drive product decisions.

The Goal Is Prioritization

The objective is not to react to every claims trend. It is to identify the signals most likely to affect pricing adequacy, underwriting performance, coverage effectiveness, or portfolio sustainability.

Insurers that establish clear decision triggers can respond more consistently and avoid both overreacting to noise and underreacting to meaningful change.

Conclusion

Claims data is no longer just a record of past losses. It is becoming a product strategy asset for insurers that want to understand how risk is changing in real time.

The real advantage is not having claims data, every carrier has it. The advantage comes from detecting meaningful signals faster and turning them into product, pricing, and underwriting decisions before issues affect profitability or portfolio performance.

As an insurance strategic consultant, Practo Insura helps carriers, MGAs, and reinsurers connect claims intelligence with product strategy, underwriting discipline, and modernization initiatives, helping them build more adaptive products for changing risk conditions.

We specialize in developing innovative Property & Casualty (P&C) insurance software solutions, leveraging over 8 years of InsurTech expertise to simplify insurance operations and enhance efficiency.

Share Article via

Subscribe to our insights newsletter

Related Blog Posts

Insurance Underwriting Automation: Implementation Guide...

12 Jun, 2026

12 Jun, 2026

Most P&C underwriters did not join the industry to chase...

Read More

What Is Subscription Auto Insurance...

15 Apr, 2026

Auto insurance was designed for a market built on long-term...

Read More

What Is Pay How You Drive Auto...

03 Apr, 2026

Auto insurance pricing is already moving beyond fixed assumptions. Over...

Read More