Auto insurance was designed for a market built on long-term vehicle ownership, predictable driving habits, and fixed policy terms.

But mobility is changing. Consumers now expect simpler billing, faster servicing, and models that align with how they access and use vehicles. As subscription-based experiences expand across industries, insurance is also beginning to shift from a rigid annual product to a more adaptable, service-led model.

That is where subscription auto insurance is gaining relevance. It gives insurers a way to align coverage with modern mobility expectations while offering customers a more flexible and convenient experience.

Understanding Subscription Auto Insurance

Subscription auto insurance is more than a shorter policy term. It is a different way of offering coverage.

Instead of putting customers into a fixed 6- or 12-month contract, this model usually works on a monthly recurring basis. Customers pay a flat monthly amount, coverage renews automatically, and changes like cancellation, upgrades, or vehicle swaps are meant to be much easier to handle.

What makes this model different is the way it is structured. Traditional auto insurance is built around a one-time policy purchase that is reviewed later at renewal. Subscription insurance is structured as a continuously active coverage model rather than a fixed-term contract.

It can be offered in two main ways:

- as a standalone monthly insurance product

- as part of a larger mobility package

That larger package may include:

- vehicle access

- maintenance

- roadside assistance

- insurance coverage under one monthly payment

This changes the role of insurance. Instead of being a separate product customers buy on its own, it becomes part of a broader mobility experience.

This also sets it apart from PAYG and PHYD models. PAYG is based on how much a person drives. PHYD is based on how a person drives. Subscription auto insurance is different because it is built around flexibility, simplicity, and convenience, not mileage tracking or behavioral scoring.

So, subscription auto insurance is not just a pricing change. It is a product and distribution model that makes coverage easier to package, manage, and deliver in a more service-driven way.

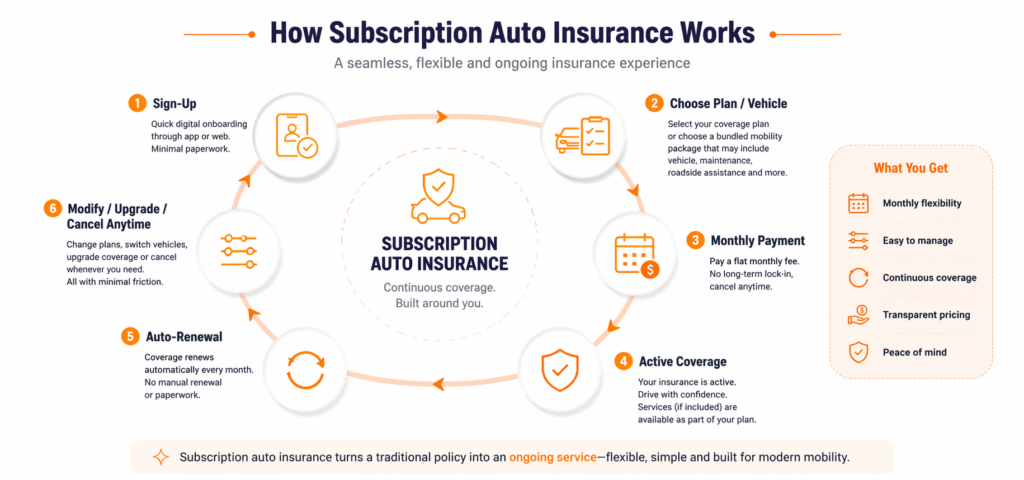

How Subscription Auto Insurance Works

Subscription auto insurance is designed to make coverage easier to start, manage, and continue.

In most cases, the journey begins digitally. Customers sign up online, choose a vehicle or coverage plan, and pay a flat monthly fee. Once activated, coverage renews automatically each month unless the customer decides to change or cancel it.

A typical customer journey looks like this:

- sign up through an app or website

- choose a vehicle, coverage tier, or bundled plan

- pay a monthly subscription fee

- start coverage immediately or on the selected date

- renew automatically each month

- upgrade, switch, or cancel with minimal friction

This makes the experience feel simpler than a traditional auto policy. Instead of managing a long-term insurance contract, the customer interacts with coverage as an ongoing monthly service.

How to Design a Subscription Pricing Model That Works

Pricing subscription auto insurance is not just about setting a monthly fee. The real challenge is designing a model that feels simple and predictable for customers, while still being financially sustainable for the insurer.

Unlike traditional policies, you are not pricing a fixed-term contract. You are pricing an ongoing relationship where customers can change plans, vehicles, and coverage more frequently. That makes pricing more sensitive to churn, duration, and usage patterns over time.

Core Pricing Models Used in Subscription Insurance

| Pricing Approach | How it Works | Best for | Main Advantage | Main Risk |

|---|---|---|---|---|

| Flat monthly pricing | One recurring fee for a standard coverage package | Simple direct-to-consumer offerings | Easy to understand and market | Can underprice risk if segmentation is weak |

| Tiered subscription plans | Multiple monthly plans based on coverage/service level | Insurers wanting flexibility without too much complexity | Supports upsell and clearer customer choice | Requires careful product design across tiers |

| Bundled pricing | Insurance included with vehicle/services in one fee | OEM, car subscription, mobility partnerships | Strong convenience and embedded distribution | Margin visibility and partner cost allocation can get difficult |

What Insurers Must Build Beneath the Monthly Price

Even if the monthly price looks simple to the customer, the pricing logic underneath needs to be carefully structured.

- Base monthly premium logic: Define the recurring price based on coverage level, vehicle category, and target segment. It should be built for a subscription model, not created by simply splitting an annual premium into 12 parts.

- Risk segmentation: Adjust pricing internally using factors like driver profile, geography, and vehicle type. This keeps pricing disciplined without making the customer experience feel complex.

- Bundle cost allocation: Separate the insurance portion from vehicle access or other bundled services. This is important for understanding true margins and avoiding hidden profitability issues.

- Mid-cycle pricing rules Set clear logic for vehicle swaps, plan upgrades, downgrades, or coverage changes during the subscription period. These changes should be handled smoothly without unnecessary friction.

- Proration logic: Calculate fair charges when customers make changes mid-month. This helps maintain billing accuracy while reducing revenue leakage.

Designing Pricing for Flexibility (Where Most Models Fail)

Subscription models break down when pricing cannot adapt to real-world behavior.

Your pricing design must support:

- frequent customer changes without manual intervention

- real-time or near real-time plan adjustments

- consistent billing despite mid-cycle modifications

- smooth transitions between plans or vehicles

If these are not built into pricing logic, operational friction quickly erodes the customer experience.

How to Evaluate Pricing Performance

Subscription auto insurance cannot be evaluated using traditional annual metrics alone. Performance needs to be tracked continuously, with a focus on customer behavior over time.

- Customer Lifetime Value (LTV): Measures the total value a customer generates over their full subscription period. This should factor in premium collected, claims cost, servicing cost, and retention duration. A strong model ensures LTV consistently exceeds acquisition and servicing costs.

- Monthly Churn Rate: Tracks the percentage of customers who cancel each month. Even small increases in churn can significantly reduce profitability, especially if acquisition costs are high.

- Average Subscription Duration: Indicates how long customers typically stay active. Longer durations improve profitability by spreading acquisition and onboarding costs over time. It also signals whether the product is delivering sustained value.

- Loss Ratio by Customer Cohort: Instead of looking only at overall loss ratios, insurers should track performance by customer groups (e.g., new vs retained customers, plan tiers, acquisition channels). This helps identify where risk or pricing issues are concentrated.

- Revenue Stability (Monthly Premium Consistency): Measures how predictable monthly income is across the portfolio. High volatility may indicate pricing gaps, churn issues, or overexposure to short-term customers.

- Plan Mix and Upgrade/Downgrade Trends: Tracks how customers move between pricing tiers. This helps insurers understand whether higher-value plans are being adopted and where revenue leakage may occur.

Operational Model Requirements for Subscription Insurance

Subscription auto insurance may feel simple to the customer, but it creates a more demanding operating model for the insurer.

Traditional auto insurance follows a fixed sequence: quote, bind, issue, then renew at the end of the policy term. Subscription models work differently. They run on a continuous lifecycle, where coverage is renewed monthly and customers may change plans, vehicles, or service levels far more often.

That means insurers cannot rely on operations designed for static policy administration. They need processes built for ongoing change.

Core Operational Capabilities

To run this model effectively, insurers need a few capabilities in place.

- Recurring billing and invoicing: The system must support monthly collections, payment retries, and proration when customers make changes mid-cycle.

- Rolling policy lifecycle management: Coverage needs to be managed as an active, ongoing service rather than a policy that only changes at renewal.

- Fast activation and deactivation: Customers expect coverage to start, stop, or switch quickly, without manual delays or back-office bottlenecks.

- Mid-cycle change handling: Operations must support vehicle swaps, plan upgrades, downgrades, and coverage edits at any point in the subscription period.

- Customer self-service support: Policyholders should be able to manage payments, plan changes, and account updates through digital channels without depending on manual support for every request.

Key Operational Risk Areas

The flexibility that makes subscription insurance attractive also creates operational pressure.

- Billing failures can disrupt active coverage: A missed or failed payment is not just a finance issue. If not handled properly, it can create coverage gaps, customer disputes, and compliance concerns.

- High churn increases processing volume: Frequent onboarding, offboarding, and account changes raise operational workload and can quickly strain teams that are still built around annual policy cycles.

- Bundled services increase coordination risk: When insurance is packaged with vehicle access, maintenance, or roadside services, multiple systems and partners must remain synchronized. If they do not, customer experience and margin control both suffer.

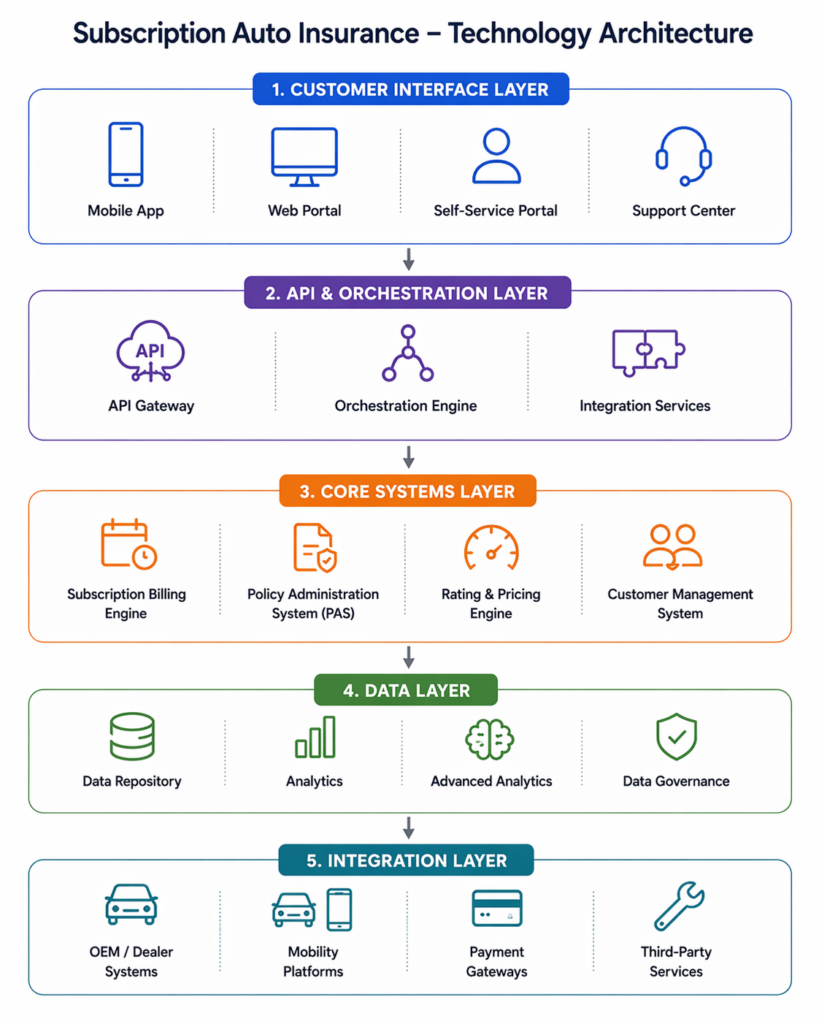

Technology Requirements for Subscription Auto Insurance

Subscription auto insurance cannot run effectively on traditional policy systems alone. The model depends on continuous updates, recurring billing, and real-time flexibility, which most legacy systems are not designed to handle.

To support this, insurers need a technology stack that enables ongoing policy orchestration, not just one-time policy issuance.

Core Technology Capabilities

To build and scale a subscription model, insurers should focus on these key components:

- Policy systems that support incremental updates:Policy administration system should allow vehicle swaps, plan changes, and coverage edits without requiring full re-issuance or manual intervention. Systems built only for fixed-term policies will struggle with this level of change.

- Billing systems designed for continuous adjustments: Monthly billing alone is not enough. The system must handle proration, failed payments, retries, and mid-cycle changes accurately and consistently at scale.

- Pricing engines that respond to event-based triggers: Rating logic should be able to update pricing when customers make changes, not just at quote or renewal. This includes plan upgrades, vehicle changes, and coverage modifications.

- Integration layers that support real-time coordination: If the product connects with OEM platforms, mobility providers, or third-party services, integrations need to be API-first and responsive. Delays between systems can create billing mismatches and poor customer experience.

- Customer platforms that enable self-service: Customers should be able to manage subscriptions, payments, and changes without manual support. This requires tightly connected front-end and core systems.

- Data systems that track behavior over time: Subscription models require visibility into churn, plan movement, and cohort performance. Data systems need to support continuous tracking, not just periodic reporting.

Integration Requirements

Subscription auto insurance rarely operates as a standalone system. In many cases, it sits inside a broader mobility ecosystem, which means insurers need strong integration across both internal and external platforms.

At a minimum, the technology stack should connect with:

- vehicle subscription platforms

- OEM and dealer systems

- mobility or ride-sharing applications

- payment gateways and billing providers

These integrations are essential for keeping pricing, billing, policy changes, and customer experience aligned across the full journey. If systems do not stay synchronized, even a well-designed product can create friction for both the insurer and the customer.

Related Read: How to Build Right Core Technology Stack for P&C Insurer in the USA

How Underwriting Changes in Subscription Auto Insurance

Underwriting in subscription auto insurance needs to work in a more dynamic environment, where coverage may change more often and customer relationships may be shorter or less stable over time. Instead of relying mainly on fixed-term assumptions, insurers need underwriting rules that can support ongoing adjustments while still protecting portfolio quality.

In practice, the biggest changes show up in a few areas:

- Eligibility needs to be tighter upfront: Clear rules are needed for which driver profiles, vehicle types, and coverage combinations are suitable. This prevents high-variability risks from entering a model designed for speed and flexibility.

- Re-rating becomes more event-driven: Pricing and underwriting should be reassessed when key changes occur, such as vehicle swaps, plan upgrades, or coverage edits. Trigger-based logic helps manage these changes without slowing down the experience.

- Shorter exposure periods need closer monitoring: Profitability can shift faster when customers stay for shorter durations. For example, a customer subscribing for one month and filing a claim early in the cycle can significantly impact margins.

- Entry and exit behavior matters more: Customers may activate coverage during high-usage periods and cancel afterward. Monitoring these patterns is critical to avoid adverse selection.

- Portfolio monitoring becomes more important: Underwriting needs to track performance by cohort, plan type, segment, vehicle category, and subscription duration to identify weak patterns early and adjust rules accordingly.

The key change is that underwriting becomes less about one-time risk assessment and more about managing risk across a product that is designed to stay flexible.

How Claims Management Needs to Change in Subscription Auto Insurance

Claims management in a subscription model needs to be built for speed, continuity, and coordination, not just settlement. Because customers can enter, exit, or modify coverage more frequently, the claims function has to operate in a way that support a model with frequent policy updates and shorter customer lifecycles.

In practical terms, insurers should focus on the following changes:

- Faster FNOL and intake workflows: Claims reporting should be instant and digital-first, with minimal steps. This reduces friction at the most critical moment and aligns with the overall subscription experience.

- Early-stage claim tracking and controls: Claims occurring soon after activation should be monitored closely, as they have a higher impact on profitability. This requires better visibility into claim timing relative to subscription start.

- Integrated service workflows: Claims systems need to connect directly with repair networks, roadside assistance, and service partners. This ensures faster resolution and avoids delays caused by disconnected processes.

- Real-time status and communication: Customers should be able to track claim progress, upload documents, and receive updates digitally. Lack of visibility can quickly impact satisfaction and retention.

- Cohort-based claims analysis: Instead of only tracking overall claims performance, insurers should analyze claims by plan type, vehicle category, acquisition channel, and subscription duration to identify patterns early.

- Flexible claims handling rules: The system should support policy changes during the claims lifecycle, such as plan upgrades or cancellations, without creating operational conflicts or manual intervention.

The key shift is that claims management needs to move from a linear, process-driven function to a more connected, real-time service layer that supports both operational efficiency and customer experience.

Regulatory Considerations for Subscription Auto Insurance

Subscription auto insurance introduces flexibility on the product side, but regulatory frameworks are still largely built around fixed-term policies. That creates a gap insurers need to manage carefully when designing and launching this model.

The goal is not just compliance, but ensuring that flexibility does not create regulatory risk, filing delays, or approval challenges across states.

Key Areas Insurers Need to Address

- Monthly renewal structure: Regulators may require clarity on how continuous monthly renewals are defined, whether they are treated as new policies, extensions, or a rolling contract. This impacts filings, disclosures, and compliance obligations.

- Cancellation and notice requirements: Even if the product allows easy cancellation, insurers must still comply with state-specific notice periods, non-renewal rules, and consumer protection requirements.

- Minimum coverage duration rules: Some jurisdictions may not fully support very short-term or highly flexible coverage structures. Insurers need to ensure the product aligns with minimum term expectations where applicable.

- Disclosure for bundled offerings: When insurance is packaged with vehicle access or other services, regulators may require clear separation and disclosure of:

– insurance vs non-insurance components

– pricing breakdown

– coverage terms and conditions - Filing and approval complexity: Subscription models often involve new pricing structures, billing logic, and product definitions. This can lead to:

– more detailed filings

– higher likelihood of objections

– longer approval timelines

Customer Strategy for Subscription Auto Insurance

Subscription auto insurance requires a different approach to customer strategy. Success depends not just on who you target, but on how the product fits into changing mobility needs and how clearly that value is delivered over time.

The model works best with customers whose mobility patterns are variable rather than fixed, and who are open to managing coverage as part of an ongoing service.

Target Segments to Focus On

Insurers should prioritize segments where variability in usage creates a natural fit:

- Urban and semi-urban drivers: More likely to have inconsistent driving patterns and changing vehicle needs

- Younger, digitally comfortable users: More open to managing products through apps and recurring payment models

- Subscription-oriented consumers: Already familiar with managing services through monthly payments

- Users of car subscription or leasing platforms: More likely to adopt bundled offerings where insurance is part of a broader package

- Convenience-driven, higher-income segments: Less price-sensitive and more focused on ease of management

How Insurers Should Approach Go-to-Market

Subscription auto insurance requires a different go-to-market approach compared to traditional policies.

- Embedded and partner-led distribution is a strong fit: The model aligns naturally with OEM platforms, vehicle subscription providers, and mobility ecosystems where insurance can be offered as part of a broader service

- Direct-to-consumer works when the product is simple: Clear pricing tiers and minimal configuration are critical for direct channels

- Acquisition should focus beyond price: Customers evaluate onboarding experience, billing clarity, and ease of use, not just premium levels

What Drives Customer Adoption in This Model

Adoption depends on how clearly the product fits into real usage and expectations:

- Clarity in what is included vs excluded: Customers need a clear understanding of what the monthly price covers, especially in bundled offerings

- Confidence in making changes without penalty: The ability to switch plans or vehicles without unexpected costs builds trust

- Consistency across the lifecycle: The experience from onboarding to claims should feel aligned, not fragmented

- Perceived control over the product: Customers should feel they can adjust coverage as their needs change without added complexity

Why Retention Matters More Than Acquisition

In this model, long-term value is driven more by how long customers stay than how many are acquired.

Insurers should actively manage:

- early churn, especially in the first few months

- engagement through ongoing interaction points

- clear pathways for plan upgrades or transitions

- service quality across claims and support

A customer who stays longer contributes significantly more value than one who frequently enters and exits.

When Subscription Auto Insurance Makes Sense for P&C Insurer

Subscription auto insurance is not the right fit for every insurer or every market. Before building it, insurers should assess whether the model aligns with their customer base, product design, operating model, and technology capabilities.

Decision Framework for Insurers

| Decision Area | What to Assess | Strong Fit Indicators | Warning Signs |

|---|---|---|---|

| Market fit | Whether customer demand supports a flexible monthly model | Urban or hybrid-driving markets, digital-first users, demand for convenience and lower commitment | Customers still prefer fixed annual policies and traditional billing |

| Product fit | Whether the product can be simplified into a recurring subscription structure | Standardized coverage tiers, simple monthly packaging, bundling potential | Highly customized products, complex rating structures, niche underwriting needs |

| Operational readiness | Whether internal teams can support frequent changes and continuous servicing | Ability to handle monthly billing, mid-cycle changes, fast activation, and self-service support | Heavy manual processing, slow servicing workflows, limited billing flexibility |

| Technology readiness | Whether core systems can support a subscription-based model | Modular PAS, recurring billing, real-time pricing, API integrations | Legacy systems built around fixed terms, batch processing, and limited integration |

| Regulatory fit | Whether the product can work within state-specific compliance requirements | Clear filing path, manageable disclosure needs, flexibility within target states | Unclear treatment of rolling renewals, strict cancellation rules, complex filing risk |

This model makes the most sense when there is alignment across all five areas. If one or two areas are weak, insurers may still explore the concept, but the launch path will likely be slower and more complex.

Strategic Takeaway

Subscription auto insurance is not just a product innovation. It is a business model decision. The stronger the fit across market demand, product structure, operations, technology, and compliance, the more realistic the opportunity becomes.

Conclusion

Subscription auto insurance is not just a different way to structure pricing. It requires insurers to rethink how products are designed, priced, operated, and supported across the full lifecycle.

For insurers exploring this model, the challenge is not whether the concept works. The real challenge is whether the organization is ready to support the coordination it requires across pricing, operations, technology, underwriting, and compliance.

Insurers need a structured approach to assess where the model fits, what capabilities need to change, and how to build it in a way that can scale without creating operational friction.

Insurance strategic consultants such as Practo Insura help insurers define the right model, align internal capabilities, and build the foundation needed to support subscription auto insurance effectively.

In the end, subscription auto insurance will not be defined by how innovative it looks on the surface. It will be defined by how well it is designed and executed behind the scenes

We specialize in developing innovative Property & Casualty (P&C) insurance software solutions, leveraging over 8 years of InsurTech expertise to simplify insurance operations and enhance efficiency.

Share Article via

Subscribe to our insights newsletter

Related Blog Posts

Insurance Underwriting Automation: Implementation Guide...

12 Jun, 2026

12 Jun, 2026

Most P&C underwriters did not join the industry to chase...

Read More

Why Claims Data Matters in...

03 Jun, 2026

Claims data has traditionally been treated as a record of...

Read More

What Is Pay How You Drive Auto...

03 Apr, 2026

Auto insurance pricing is already moving beyond fixed assumptions. Over...

Read More