Usage-based insurance (UBI) has quietly become a core part of auto strategy, not a side experiment.

Straits Research estimates the global UBI market at USD 33.47 billion in 2025, growing to USD 122.33 billion by 2034 at a 15.9% CAGR. North America holds about 35% of that, and the U.S. UBI market alone is around USD 11.76 billion in 2024, rising to USD 13.05 billion in 2025. In other words, telematics-based auto products are now firmly mainstream in P&C.

The question is no longer “Should we do UBI?” but “How do we evolve our program so it’s competitive, compliant, and scalable?”

The State of UBI Today – Useful, But Still Underpowered

Most U.S. P&C auto carriers still run UBI in roughly the same way: telematics data from a smartphone app or OBD dongle, simple signals like miles, speeding, harsh braking and time of day, used mainly for discounts or surcharges in personal auto across a limited set of states.

At the same time, state DOIs are paying closer attention to big data, AI and telematics in line with NAIC guidance, while GLBA and CCPA/CPRA are tightening consent, data minimization and disclosure requirements.

States like California (Prop 103) sharply restrict how driving-behavior data can be used for rating, pushing carriers to maintain different playbooks for “pricing states” and “coaching-only states.” UBI clearly delivers value, but in many books it’s still underpowered relative to its potential and to the regulatory risk it now attracts.

7 UBI Trends in Auto Insurance and How to Adopt Them

1. Smarter Risk Scoring with AI

Many programs still rely on relatively simple scoring formulas: distance driven, number of harsh braking events, a speeding index, maybe time of day. These are useful, but they underuse the richness of modern telematics.

Future Trend: AI-native scoring using richer context

Leading telematics and insurtech players are moving to machine-learning models that consider:

- Speed vs posted limit and road type

- Time and location risk (night, high-crash corridors)

- Weather and traffic conditions

- Mobile distraction signals

- Trip context patterns (commute vs irregular trips)

This allows much finer risk separation between, say, two 10,000-mile-per-year drivers — one who drives mostly calm suburban routes at off-peak hours, and one whose pattern is late-night, congested, high-risk corridors.

How U.S. P&C auto insurers can make the shift

- Build a telematics data foundation

Set up a basic trip-level and event-level store in your existing data lake/warehouse with a consistent schema. Ensure every trip can be reliably linked to policies, vehicles, and drivers under clear consent and privacy controls. - Start in shadow mode

Keep the current approved telematics score for rating but run ML-based scores in parallel on a subset of policies to compare stability, lift, and fairness. - Embed model governance from day one

Document variables, assumptions, and exclusions clearly, and involve compliance, actuarial, and legal early, especially in stricter states.

2. From Dongles-Only to OEM + Smartphone Hybrid Data

Many programs still run on plug-in OBD devices or entirely on smartphone sensors. Both can work, but each has pain points: logistics and cost for dongles, data quality and battery concerns for phones.

Future Trend: Connected car/OEM data as the default

Many newer vehicles roll off the line with embedded telematics hardware and connectivity. OEMs and data aggregators now expose vehicle data via APIs, including odometer, ignition, location, certain ADAS events, and sometimes crash indicators.

The near future looks hybrid:

- OEM data as the primary source for compatible vehicles

- Smartphone apps adding UX, coaching, and supplementary signals

- OBD dongles fading except where necessary

How to Add OEM Data Without Rebuilding Everything

- Partner, don’t build from scratch

Integrate with one or more OEM data platforms/aggregators instead of negotiating one-off OEM deals. - Redesign consent and onboarding flows

At quote/bind, clearly explain what data you collect, the legal basis (e.g., consent under CCPA/CPRA), and whether it’s for pricing, coaching, or claims. - Offer clear product variants

Create “Connected-car UBI” for compatible vehicles (low friction) and “App-only UBI” for others. Consider a hybrid model where the car provides core data while the app handles engagement, coaching, and notifications.

Done right, OEM-powered UBI can reduce device costs, improve participation rates, and create a path to real-time services like crash notifications and enhanced FNOL.

3. UBI for Everyday Drivers, Fleets, and New Mobility

Most programs focus on private passenger auto in a limited set of states. Small commercial, fleets, and new mobility (rideshare, delivery, scooters, shared vehicles) are often serviced with traditional products.

Future Trend: UBI as the fabric of mobility risk

Straits projects Asia-Pacific as the fastest-growing UBI region (~17.45% CAGR), with North America still leading overall share. Much of that growth is in fleets, shared mobility and OEM-integrated offerings.

For U.S. P&C carriers, that translates into:

- Small commercial fleets (contractors, delivery, trades) with telematics baked in

- Embedded coverage for rideshare and gig economy drivers

- EV and charging ecosystem partnerships

- Multi-state expansion with configurable telematics features

How to Extend UBI from Personal Auto into Fleets and Platforms

- Start by adding UBI features to small commercial auto where you already have distribution.

- Expose APIs so partners (MGAs, fleets, platforms) can enroll drivers and access scores.

- Design filings and products so telematics components can be switched on/off by state and channel

Related Read: What Is Pay-As-You-Go Auto Insurance?

5. Different UBI Plans for Different Drivers

A single telematics program is often used for everyone, with minor tweaks. A teenager, a retiree, and a delivery driver could be in essentially the same construct.

Future Trend: Segment-specific UBI products

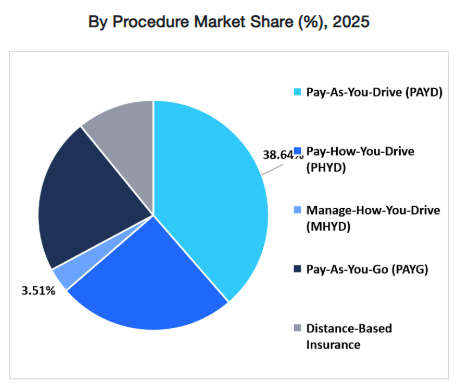

Straits’ segmentation confirms what many P&C insurers already see: PAYD dominates current UBI policy types, but other variants such as Pay-How-You-Drive (PHYD), Manage-How-You-Drive (MHYD), and distance-based models are growing alongside new applications like commercial insurance and shared mobility platforms.

Leading auto carriers and insurtechs are carving out focused propositions:

- Young driver safety programs (parent dashboards, curfews, curfew alerts)

- Low-mileage pay-per-mile products

- Gig and delivery drivers (focus on exposure, route risk, fatigue)

- EV-specific products (eco-driving, battery health, regenerative braking use)

- Small commercial fleets (dashboards, driver ranking, coaching for fleet managers)

How to Design UBI Offers by Driver Segment

- Build a simple UBI product matrix

List key segments such as rows (young drivers, low mileage, EV owners, small fleets) and key levers as columns (pricing logic, underwriting rules, UX features, distribution). This makes it clear which segments you’re serving, how, and where gaps or overlaps exist. - Start with one or two anchor segments

For example, low-mileage urban drivers and EV owners are often receptive to telematics and price-for-usage models. - Align filings and segmentation logic

Ensure your rating plans, underwriting guidelines, and marketing messaging are aligned, especially for admitted products.

Segmenting this way helps you avoid a “blob product” that works okay for everyone but delights no one.

5. Using Driving Data Beyond Just Pricing

In many carriers, telematics data is used almost exclusively by pricing and product. Claims, SIU, and retention teams either don’t have access or don’t have workflows built around it.

Future Trend: Telemetry as a shared asset across the value chain

The same data can:

- Trigger crash detection and enhanced FNOL

- Support liability decisions with pre- and post-impact speed/braking patterns

- Power fraud rules (impossible journeys, inconsistent impacts)

- Inform retention (worsening scores, disengaged users) and cross-sell

How to Plug Telematics into Claims, Fraud, and Service

- Map where telematics belongs beyond rating

Identify 2–3 non-pricing use cases and build narrow pilots such as in claims for FNOL, liability assessment, or for SIU in anomaly detection. - Build controlled use cases first

Start with opt-in crash notifications and improved FNOL workflows. Then move into SIU referral rules based on well-defined anomalies. - Clarify and disclose usage in your notices and filings

Your privacy notices and consent flows should cover all purposes for which telematics data may be used, not just pricing.

The goal: make telematics a shared analytic asset that improves combined ratio across underwriting, claims, and retention, not just a rating gimmick.

6. From Discount Program to Prevention & Coaching

For many carriers, UBI is still primarily a discount engine. Customers enroll, drive for a few months, then get a renewal discount or surcharge. Engagement is minimal, and many policyholders forget they’re even in a program.

Future Trend: Behavior change and safety as core value

UBI is also about changing driving behavior, not just measuring it. That means:

- Real-time or near real-time feedback on trips

- Weekly “driving health” summaries

- Challenges and gamified incentives

- Rewards for consistent improvement, not just one-off good weeks

How Insurers Can Turn UBI into a Coaching Experience

- Build a basic UX loop: onboarding → trip feedback → weekly summaries → renewal view.

- Test rewards like fuel vouchers or small premium credits using A/B experiments.

- Talk about UBI as a safety coach plus fair pricing, not just a discount lottery.

Related Read: What Is Pay How You Drive Auto Insurance?

7. Making UBI Clear, Fair, and Privacy-Safe

Many programs still feel opaque to customers with long privacy policies nobody reads, scores that change without clear explanation and confusion about what data is captured (location, speed, passengers).

Future Trend: Transparent, audited, and privacy-conscious design

Regulators are increasingly focused on algorithmic fairness, data minimization, and explainability, especially when models touch protected classes or proxy variables.

How to Build Explainable, Compliant UBI Models

- Create layered privacy notices (short summary + detailed legal text) that spell out data categories, purposes, retention, and sharing.

- Give drivers simple, structured feedback: “Your score dropped mainly due to late-night trips and frequent hard braking on three journeys.”

- Run fairness tests on models and document mitigation steps for internal model risk committees and future DOI queries.

This is not just about avoiding fines or bad headlines. Transparent, privacy-safe design is also a commercial advantage in a market where consumers are increasingly wary of data-driven products.

Conclusion

Usage-based insurance is no longer a novelty that carriers can experiment with on the side. For U.S. P&C and auto insurers, it’s quickly becoming a strategic asset, offering:

- A richer, more timely view of driving risk

- A way to reward and retain the right customers

- A data spine that connects pricing, claims, fraud, and retention

- A testbed for AI and advanced analytics under real regulatory constraints

An insurtech partner like Practo Insura can help U.S. P&C insurers design that roadmap end to end, from telematics data foundations and AI-driven scoring to compliant multi-state filings and real-world UBI pilots. The carriers that win won’t be the ones with the flashiest models, but the ones that move deliberately and steadily: starting with a clear plan, proving value in controlled pilots, working closely with regulators, and building lasting trust with their drivers.

We specialize in developing innovative Property & Casualty (P&C) insurance software solutions, leveraging over 8 years of InsurTech expertise to simplify insurance operations and enhance efficiency.

Share Article via

Subscribe to our insights newsletter

Related Blog Posts

Insurance Underwriting Automation: Implementation Guide...

12 Jun, 2026

12 Jun, 2026

Most P&C underwriters did not join the industry to chase...

Read More

Why Claims Data Matters in...

03 Jun, 2026

Claims data has traditionally been treated as a record of...

Read More

What Is Subscription Auto Insurance...

15 Apr, 2026

Auto insurance was designed for a market built on long-term...

Read More